问题如下图:

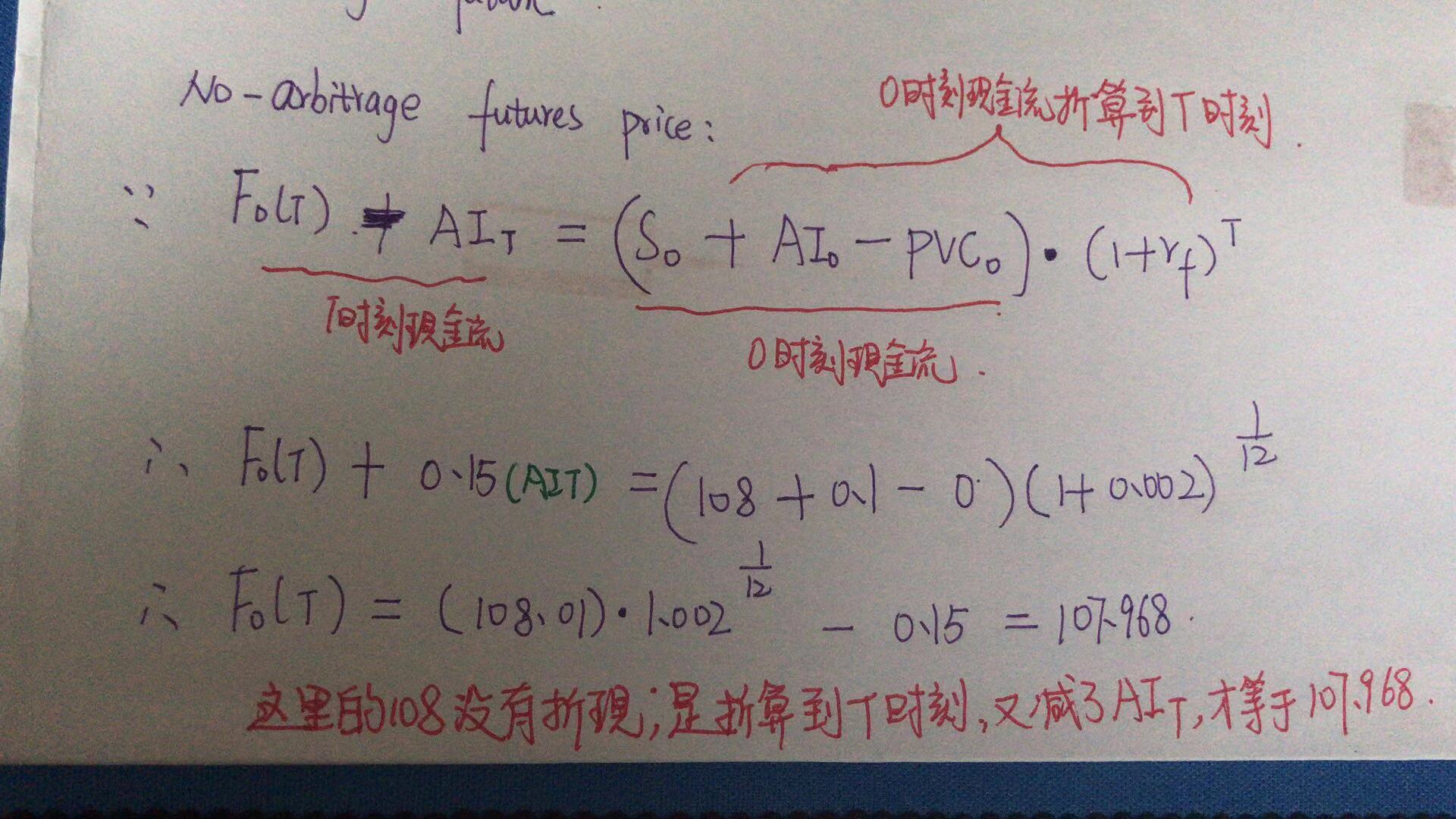

老师,看不懂答案,时间点有点搞不清楚,108不是已经折现了吗?到107.968,为啥又折现一遍?

老师,看不懂答案,时间点有点搞不清楚,108不是已经折现了吗?到107.968,为啥又折现一遍?

选项:

A.

B.

C.

解释:

NO.PZ2019010402000001 问题如下 A trar is looking for arbitrage opportunity relating to a bonfutures baseon following information: Quotefutures price=103 Conversion factor=1.02 One month remaining to expiration, no coupon ring this perio Quotebonprice=108 AI0=0.1 AIT=0.15 Annucompounrisk-free rate=0.2%The arbitrage profit is closest to: A.0.8965 B.2.9075 C.1.3253 B is correct.考点fixeincome futures定价解析:No-arbitrage futures price:F0(T) =(108+0.1) (1 + 0.002)1/12-0.15=107.968市场中的futures price=quotefutures pri* CF=103*1.02=105.06arbitrage profit应该是两个futures price之差的现值所以arbitrage profit= (107.968−105.06)(1+0.2%)1/12=2.9075\frac{(107.968-105.06)}{{(1+0.2\%)}^{1/12}}=2.9075(1+0.2%)1/12(107.968−105.06)=2.9075求No-arbitrage futures price画图:(该题合约期间没有coupon,所以PVC=0) 能否下题目中每个条件分别代表具体什么意思?

NO.PZ2019010402000001 问题如下 A trar is looking for arbitrage opportunity relating to a bonfutures baseon following information: Quotefutures price=103 Conversion factor=1.02 One month remaining to expiration, no coupon ring this perio Quotebonprice=108 AI0=0.1 AIT=0.15 Annucompounrisk-free rate=0.2%The arbitrage profit is closest to: A.0.8965 B.2.9075 C.1.3253 B is correct.考点fixeincome futures定价解析:No-arbitrage futures price:F0(T) =(108+0.1) (1 + 0.002)1/12-0.15=107.968市场中的futures price=quotefutures pri* CF=103*1.02=105.06arbitrage profit应该是两个futures price之差的现值所以arbitrage profit= (107.968−105.06)(1+0.2%)1/12=2.9075\frac{(107.968-105.06)}{{(1+0.2\%)}^{1/12}}=2.9075(1+0.2%)1/12(107.968−105.06)=2.9075求No-arbitrage futures price画图:(该题合约期间没有coupon,所以PVC=0) 为什么不用自然对数折现

NO.PZ2019010402000001 问题如下 A trar is looking for arbitrage opportunity relating to a bonfutures baseon following information: Quotefutures price=103 Conversion factor=1.02 One month remaining to expiration, no coupon ring this perio Quotebonprice=108 AI0=0.1 AIT=0.15 Annucompounrisk-free rate=0.2%The arbitrage profit is closest to: A.0.8965 B.2.9075 C.1.3253 B is correct.考点fixeincome futures定价解析:No-arbitrage futures price:F0(T) =(108+0.1) (1 + 0.002)1/12-0.15=107.968市场中的futures price=quotefutures pri* CF=103*1.02=105.06arbitrage profit应该是两个futures price之差的现值所以arbitrage profit= (107.968−105.06)(1+0.2%)1/12=2.9075\frac{(107.968-105.06)}{{(1+0.2\%)}^{1/12}}=2.9075(1+0.2%)1/12(107.968−105.06)=2.9075求No-arbitrage futures price画图:(该题合约期间没有coupon,所以PVC=0) 我根据解析中画图法算出来FP=102.9672,和103*1.02轧差后是2.09

NO.PZ2019010402000001 问题如下 A trar is looking for arbitrage opportunity relating to a bonfutures baseon following information: Quotefutures price=103 Conversion factor=1.02 One month remaining to expiration, no coupon ring this perio Quotebonprice=108 AI0=0.1 AIT=0.15 Annucompounrisk-free rate=0.2%The arbitrage profit is closest to: A.0.8965 B.2.9075 C.1.3253 B is correct.考点fixeincome futures定价解析:No-arbitrage futures price:F0(T) =(108+0.1) (1 + 0.002)1/12-0.15=107.968市场中的futures price=quotefutures pri* CF=103*1.02=105.06arbitrage profit应该是两个futures price之差的现值所以arbitrage profit= (107.968−105.06)(1+0.2%)1/12=2.9075\frac{(107.968-105.06)}{{(1+0.2\%)}^{1/12}}=2.9075(1+0.2%)1/12(107.968−105.06)=2.9075求No-arbitrage futures price画图:(该题合约期间没有coupon,所以PVC=0) 如题

NO.PZ2019010402000001 问题如下 A trar is looking for arbitrage opportunity relating to a bonfutures baseon following information: Quotefutures price=103 Conversion factor=1.02 One month remaining to expiration, no coupon ring this perio Quotebonprice=108 AI0=0.1 AIT=0.15 Annucompounrisk-free rate=0.2%The arbitrage profit is closest to: A.0.8965 B.2.9075 C.1.3253 B is correct.考点fixeincome futures定价解析:No-arbitrage futures price:F0(T) =(108+0.1) (1 + 0.002)1/12-0.15=107.968市场中的futures price=quotefutures pri* CF=103*1.02=105.06arbitrage profit应该是两个futures price之差的现值所以arbitrage profit= (107.968−105.06)(1+0.2%)1/12=2.9075\frac{(107.968-105.06)}{{(1+0.2\%)}^{1/12}}=2.9075(1+0.2%)1/12(107.968−105.06)=2.9075求No-arbitrage futures price画图:(该题合约期间没有coupon,所以PVC=0) 请问解答中arbitrage profit为什么要折现呢?