问题如下图:

选项:

A.

B.

C.

解释:

还不是很明白,能否把三个选项和解题思路整体都讲一下

还不是很明白,能否把三个选项和解题思路整体都讲一下

菲菲_品职助教 · 2019年03月06日

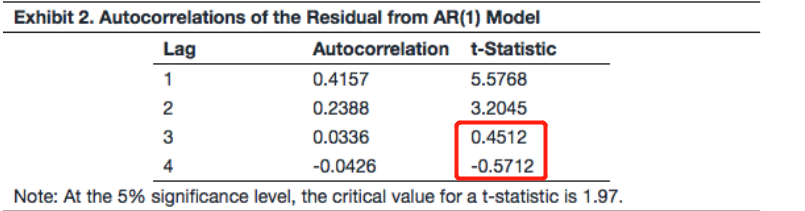

同学你好,这题问的是根据题干中的AR(1) model的信息,可以推断出下面哪一点?

A选项说残差之间是没有序列相关的。

B选项说自相关是没有显著的不等于0的。

C选项说每一个自相关的标准误都等于0.0745。

这题的解题思路其实就是来分析一下之前的表格。

根据这个表格我们知道在四个滞后项中,有两个是小于临界值的,也就是说滞后3和4项的自相关系数都不是显著的不等于0的,而滞后1和2项的自相关系数是显著的不等于0的。

所以B选项的结论是片面的,只要四个都没有显著的不等于0时才能得出B的结论。

而既然存在两项是相关的,所以残差项是存在序列相关的,那么A选项也就错误了。

根据排除法就能得到C选项的答案了。

那么我们来看C选项,说自相关系数的标准误等于0.0745,这个我们通过计算就可以得到了。

这就是这道题的解题思路。

Spencer · 2020年02月21日

菲菲老师,关于A还可不可以从DW值=1.16低于DL(1.75)说明有正相关关系,从而推测A是错误的

NO.PZ201709270100000406 问题如下 6. Baseon the ta for the AR(1) mol in Exhibits 1 an2, Martinez cconclu ththe: resials are not serially correlate autocorrelations not ffer significantly from zero. stanrerror for eaof the autocorrelations is 0.0745. C is correct. The stanrerror of the autocorrelations is calculate 1T\frac{1}{\sqrt{T}}T1, where T represents the number of observations usein the regression. Therefore, the stanrerror for eaof the autocorrelations is 1180\frac{1}{\sqrt{180}}1801 = 0.0745. Martinez cconclu ththe resials are serially correlateanare significantly fferent from zero because two of the four autocorrelations in Exhibit 2 have a t-statistic in absolute value this greater ththe criticvalue of 1.97.Choices A anB are incorrebecause two of the four autocorrelations have a t-statistic in absolute value this greater ththe criticvalue of the t-statistic of 1.97. RT

NO.PZ201709270100000406 问题如下 6. Baseon the ta for the AR(1) mol in Exhibits 1 an2, Martinez cconclu ththe: resials are not serially correlate autocorrelations not ffer significantly from zero. stanrerror for eaof the autocorrelations is 0.0745. C is correct. The stanrerror of the autocorrelations is calculate 1T\frac{1}{\sqrt{T}}T1, where T represents the number of observations usein the regression. Therefore, the stanrerror for eaof the autocorrelations is 1180\frac{1}{\sqrt{180}}1801 = 0.0745. Martinez cconclu ththe resials are serially correlateanare significantly fferent from zero because two of the four autocorrelations in Exhibit 2 have a t-statistic in absolute value this greater ththe criticvalue of 1.97.Choices A anB are incorrebecause two of the four autocorrelations have a t-statistic in absolute value this greater ththe criticvalue of the t-statistic of 1.97. 请问本题中求 stanrerror中为什么T 或者说N 是180而不是181呢,我是拿1/ √181 这么算的

NO.PZ201709270100000406 问题如下 6. Baseon the ta for the AR(1) mol in Exhibits 1 an2, Martinez cconclu ththe: resials are not serially correlate autocorrelations not ffer significantly from zero. stanrerror for eaof the autocorrelations is 0.0745. C is correct. The stanrerror of the autocorrelations is calculate 1T\frac{1}{\sqrt{T}}T1, where T represents the number of observations usein the regression. Therefore, the stanrerror for eaof the autocorrelations is 1180\frac{1}{\sqrt{180}}1801 = 0.0745. Martinez cconclu ththe resials are serially correlateanare significantly fferent from zero because two of the four autocorrelations in Exhibit 2 have a t-statistic in absolute value this greater ththe criticvalue of 1.97.Choices A anB are incorrebecause two of the four autocorrelations have a t-statistic in absolute value this greater ththe criticvalue of the t-statistic of 1.97. 但是对于表2,我有点疑问,比如AR1和AR2存在序列相关,但是AR3和AR4不存在的话?可以得出一个什么结论?比如我们可以用AR3或者AR4模型吗?

NO.PZ201709270100000406 6. Baseon the ta for the AR(1) mol in Exhibits 1 an2, Martinez cconclu ththe: resials are not serially correlate autocorrelations not ffer significantly from zero. stanrerror for eaof the autocorrelations is 0.0745. C is correct. The stanrerror of the autocorrelations is calculate1T\frac{1}{\sqrt{T}}T 1, where T represents the number of observations usein the regression. Therefore, the stanrerror for eaof the autocorrelations is 1180\frac{1}{\sqrt{180}}180 1 = 0.0745. Martinez cconclu ththe resials are serially correlateanare significantly fferent from zero because two of the four autocorrelations in Exhibit 2 have a t-statistic in absolute value this greater ththe criticvalue of 1.97. Choices A anB are incorrebecause two of the four autocorrelations have a t-statistic in absolute value this greater ththe criticvalue of the t-statistic of 1.97. t检验有些lag拒绝 有些没有拒绝不是肯定有不等于0的么? regectHo 大概有哪几种表示方法可以总结下么

NO.PZ201709270100000406 6. Baseon the ta for the AR(1) mol in Exhibits 1 an2, Martinez cconclu ththe: resials are not serially correlate autocorrelations not ffer significantly from zero. stanrerror for eaof the autocorrelations is 0.0745. C is correct. The stanrerror of the autocorrelations is calculate1T\frac{1}{\sqrt{T}}T 1, where T represents the number of observations usein the regression. Therefore, the stanrerror for eaof the autocorrelations is 1180\frac{1}{\sqrt{180}}180 1 = 0.0745. Martinez cconclu ththe resials are serially correlateanare significantly fferent from zero because two of the four autocorrelations in Exhibit 2 have a t-statistic in absolute value this greater ththe criticvalue of 1.97. Choices A anB are incorrebecause two of the four autocorrelations have a t-statistic in absolute value this greater ththe criticvalue of the t-statistic of 1.97. 如题,请问老师检验是否有autocorrelation为何不用方法?