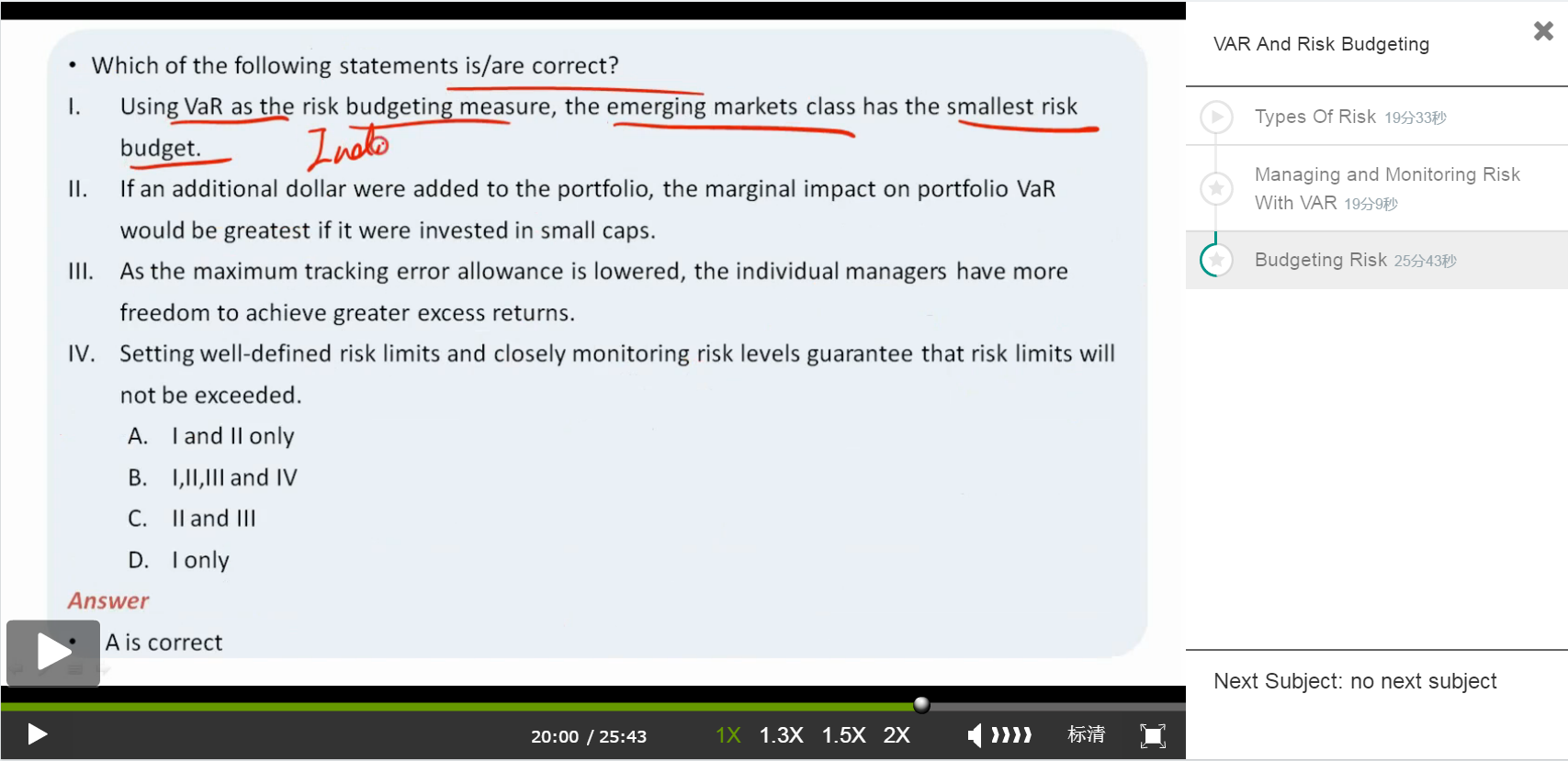

问题如下图:

选项:

A.

B.

C.

D.

解释:

Ⅰ的解释不理解,课程讲解risk budget先定好分数线,再分权重,risk budget可能都不是真实VAR,而是一个总体目标,那分解下来的为什么就可以用individual VAR来代表呢?用risk budget权重的公式来看,emerging mkt也是最小的,但不理解这个解释,谢谢!

NO.PZ2016071602000013 问题如下 The pension management analysts Big Inuse a two-step process to manage the assets anrisk in the pension portfolio. First, they use a VAR-baserisk bueting process to termine the asset allocation across four broasset classes. Then, within eaasset class, they set a maximum tracking error allowanfrom a benchmark inx antermine active risk buet to stribute among invimanagers. Assume the returns are all normally stribute From the first step in the process, the following information is available.Whiof the following statements is/are correct?I. Using Vthe risk bueting measure, the emerging markets class hthe smallest risk buet.II. If aitionllwere aeto the portfolio, the marginimpaon portfolio Vwoulgreatest if it were investein small caps.III. the maximum tracking error allowanis lowere the invimanagers have more freem to achieve greater excess returns.IV. Setting well-finerisk limits anclosely monitoring risk levels guarantee thrisk limits will not excee A.I anII only B.I,II,III,anIV C.II anIII I only A is correct. Risk buet is representethe inviVAR, whiis the smallest for emerging markets, so statement I. is correct. The marginVis highest for small caps, so aing one llto thasset class woulhave the largest impaon the portfolio. Statement III. is incorrect, lowering TEV woulgive less, not more freem to manages. Finally, setting risk limits es not ensure they will not excee Bluanexceptions chappen, even if the risk mol is correct. 老师,求问MarginVar和IncrementVar,对Statement II,为什么不是Incrementa,谢谢

NO.PZ2016071602000013 问题如下 The pension management analysts Big Inuse a two-step process to manage the assets anrisk in the pension portfolio. First, they use a VAR-baserisk bueting process to termine the asset allocation across four broasset classes. Then, within eaasset class, they set a maximum tracking error allowanfrom a benchmark inx antermine active risk buet to stribute among invimanagers. Assume the returns are all normally stribute From the first step in the process, the following information is available.Whiof the following statements is/are correct?I. Using Vthe risk bueting measure, the emerging markets class hthe smallest risk buet.II. If aitionllwere aeto the portfolio, the marginimpaon portfolio Vwoulgreatest if it were investein small caps.III. the maximum tracking error allowanis lowere the invimanagers have more freem to achieve greater excess returns.IV. Setting well-finerisk limits anclosely monitoring risk levels guarantee thrisk limits will not excee A.I anII only B.I,II,III,anIV C.II anIII I only A is correct. Risk buet is representethe inviVAR, whiis the smallest for emerging markets, so statement I. is correct. The marginVis highest for small caps, so aing one llto thasset class woulhave the largest impaon the portfolio. Statement III. is incorrect, lowering TEV woulgive less, not more freem to manages. Finally, setting risk limits es not ensure they will not excee Bluanexceptions chappen, even if the risk mol is correct. risk bueting measurement是用invivar在哪里讲到?

NO.PZ2016071602000013 问题如下 The pension management analysts Big Inuse a two-step process to manage the assets anrisk in the pension portfolio. First, they use a VAR-baserisk bueting process to termine the asset allocation across four broasset classes. Then, within eaasset class, they set a maximum tracking error allowanfrom a benchmark inx antermine active risk buet to stribute among invimanagers. Assume the returns are all normally stribute From the first step in the process, the following information is available.Whiof the following statements is/are correct?I. Using Vthe risk bueting measure, the emerging markets class hthe smallest risk buet.II. If aitionllwere aeto the portfolio, the marginimpaon portfolio Vwoulgreatest if it were investein small caps.III. the maximum tracking error allowanis lowere the invimanagers have more freem to achieve greater excess returns.IV. Setting well-finerisk limits anclosely monitoring risk levels guarantee thrisk limits will not excee A.I anII only B.I,II,III,anIV C.II anIII I only A is correct. Risk buet is representethe inviVAR, whiis the smallest for emerging markets, so statement I. is correct. The marginVis highest for small caps, so aing one llto thasset class woulhave the largest impaon the portfolio. Statement III. is incorrect, lowering TEV woulgive less, not more freem to manages. Finally, setting risk limits es not ensure they will not excee Bluanexceptions chappen, even if the risk mol is correct. No.PZ2016071602000013 (选择题)来源: HanookThe pension management analysts Big Inuse a two-step process to manage the assets anrisk in the pension portfolio. First, they use a VAR-baserisk bueting process to termine the asset allocation across four broasset classes. Then, within eaasset class, they set a maximum tracking error allowanfrom a benchmark inx antermine active risk buet to stribute among invimanagers. Assume the returns are all normally stribute From the first step in the process, the following information is available.Whiof the following statements is/are correct?I. Using Vthe risk bueting measure, the emerging markets class hthe smallest risk buet.II. If aitionllwere aeto the portfolio, the marginimpaon portfolio Vwoulgreatest if it were investein small caps.III. the maximum tracking error allowanis lowere the invimanagers have more freem to achieve greater excess returns.IV. Setting well-finerisk limits anclosely monitoring risk levels guarantee thrisk limits will not excee想问一下II,为什么没有把第一列expectereturn考虑进去呢。讲义上说increase position with higher sharpe ratio,rf是一致的,如果用expectereturn/MVaR,那么最大的应该是commoties

NO.PZ2016071602000013 I,II,III,anIV II anIII I only A is correct. Risk buet is representethe inviVAR, whiis the smallest for emerging markets, so statement I. is correct. The marginVis highest for small caps, so aing one llto thasset class woulhave the largest impaon the portfolio. Statement III. is incorrect, lowering TEV woulgive less, not more freem to manages. Finally, setting risk limits es not ensure they will not excee Bluanexceptions chappen, even if the risk mol is correct. 老师,请问4错在哪呢?

老师,statement lll,TEV越小,no more freemm to manager 怎么理解?