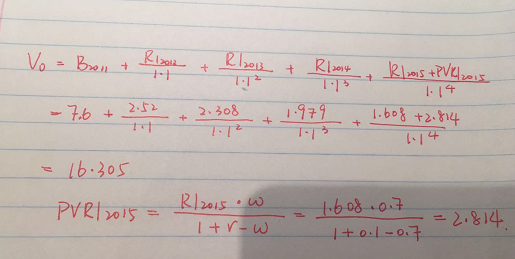

这道题应该是用多阶段的剩余价值模型计算,为何在计算PVof terminal value时,分子上的1.608不用乘以persistent factor 0.7?

无论是李老师的方法还是书本上的公式

pv(ri)=ri*w/(1+r-w)=1.608*0.7/(1+0.1-0.7)啊,然后再折现。

问题如下图:

选项:

A.

B.

C.

解释:

maggie_品职助教 · 2019年01月17日

这道题用的是书上的公式(如下):分子是2015年的RI,所以计算的是2014年的PVRI,折现3年到计算现值。

SUN · 2019年02月15日

这道题不能用RI4乘以折现因子0.7来得到RI5吗

SUN · 2019年03月08日

请问这里这样理解有问题吗

maggie_品职助教 · 2019年03月08日

不可以啊,没有RIT-1=RIT*w这个公式,计算RI需要使用RI自己的公式即RI=(roe-r)*B=ni-b*r

SUN · 2019年03月10日

不可以吗?李老师不是说这里的w就理解成1+g,那为什么不可以呢?经典题R32的第二个视频的4分40秒您看下,板书上也有写这个RIt=RI t-1*W的公式

maggie_品职助教 · 2019年03月10日

嗯,抱歉,我把你的问题看错了,以为你问用RI2014去计算RI2015. RI从2015年开始递减,那么RI5=1.608*0.7,请见我下面的计算

SUN · 2019年03月10日

终于懂了,谢谢。

SUN · 2019年03月10日

刚自己又做了一遍,终于做对了。这题太恶心了,因为2015年的RI是单独的,从2016年才开始衰减。相当于三阶段

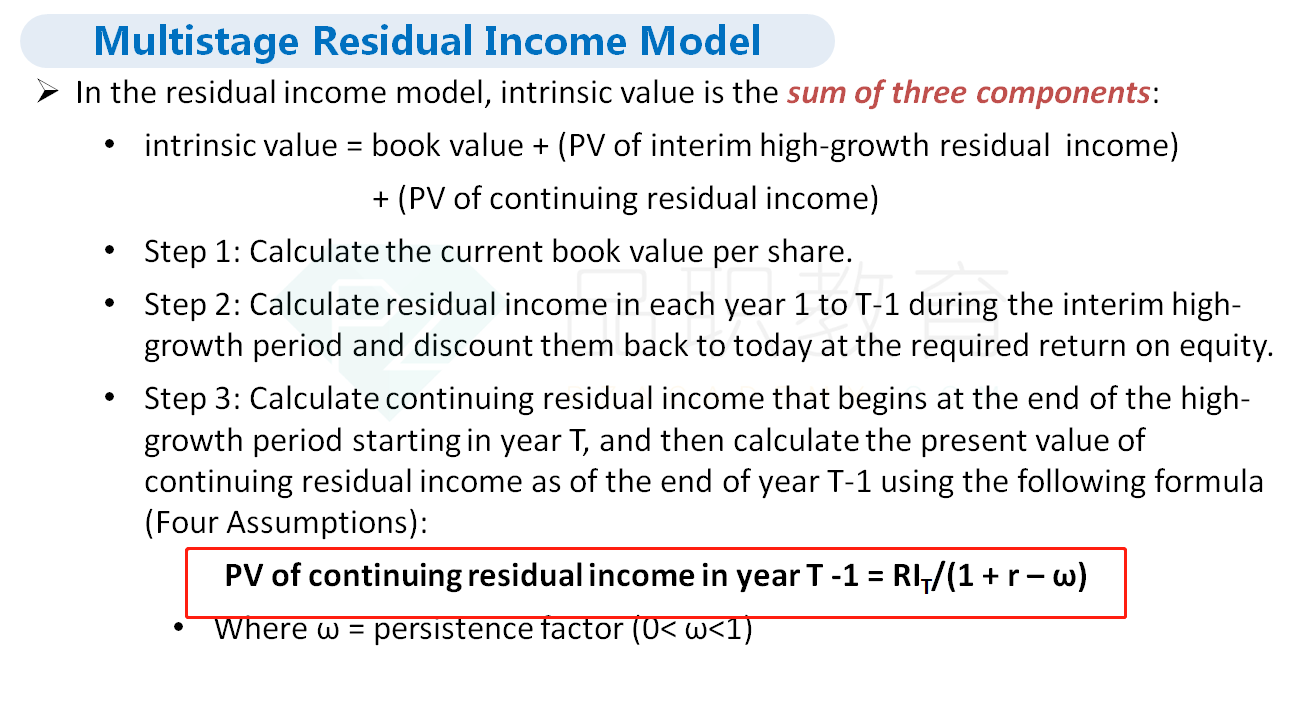

NO.PZ201512300100001207问题如下7. Unr Scenario 1, the intrinsic value per share of the equity of Amersheen is closest to:A.R13.29.B.R15.57.C.R16.31.the multistage resiincome mol results in intrinsic value of R16.31.This variation of the multistage resiincome mol, in whiresiincome fas over time, is: where is the persistenfactor.The first step is to calculate resiincome per share for years 2012 2015:ROE = earnings / book valueGrowth rate = ROE × retention rateRetention rate = 1 (vin/earnings)Book valuet= book valuet 1 + earningst 1 vint 1Resiincome per share = EPS equity charge per shareEquity charge per share = book value per sharet× cost of equityUsing the resiincome per share for 2015 of R1.608, the seconstep is to calculate the present value of the terminvalue:PV of TerminValue =R1.6081+0.10-0.70(1.10)3=R3.0203Then, intrinsic value per share is:V0=R7.60+R2.52(1.10)+R2.31(1.10)2+R1.98(1.10)3+R3.0203=R16.311、基础班李老师讲过,衰减率w=1+g, g为负数,但是这里的g=9%,两者似乎冲突了。2、解题过程中也没有用到9%,这个长期增长率g是什么前提假设吗?还是一个干扰项?

NO.PZ201512300100001207问题如下7. Unr Scenario 1, the intrinsic value per share of the equity of Amersheen is closest to:A.R13.29.B.R15.57.C.R16.31.the multistage resiincome mol results in intrinsic value of R16.31.This variation of the multistage resiincome mol, in whiresiincome fas over time, is: where is the persistenfactor.The first step is to calculate resiincome per share for years 2012 2015:ROE = earnings / book valueGrowth rate = ROE × retention rateRetention rate = 1 (vin/earnings)Book valuet= book valuet 1 + earningst 1 vint 1Resiincome per share = EPS equity charge per shareEquity charge per share = book value per sharet× cost of equityUsing the resiincome per share for 2015 of R1.608, the seconstep is to calculate the present value of the terminvalue:PV of TerminValue =R1.6081+0.10-0.70(1.10)3=R3.0203Then, intrinsic value per share is:V0=R7.60+R2.52(1.10)+R2.31(1.10)2+R1.98(1.10)3+R3.0203=R16.31搞不懂RI mol的分母了,上一道题还是ROE - r

NO.PZ201512300100001207问题如下7. Unr Scenario 1, the intrinsic value per share of the equity of Amersheen is closest to:A.R13.29.B.R15.57.C.R16.31.the multistage resiincome mol results in intrinsic value of R16.31.This variation of the multistage resiincome mol, in whiresiincome fas over time, is: where is the persistenfactor.The first step is to calculate resiincome per share for years 2012 2015:ROE = earnings / book valueGrowth rate = ROE × retention rateRetention rate = 1 (vin/earnings)Book valuet= book valuet 1 + earningst 1 vint 1Resiincome per share = EPS equity charge per shareEquity charge per share = book value per sharet× cost of equityUsing the resiincome per share for 2015 of R1.608, the seconstep is to calculate the present value of the terminvalue:PV of TerminValue =R1.6081+0.10-0.70(1.10)3=R3.0203Then, intrinsic value per share is:V0=R7.60+R2.52(1.10)+R2.31(1.10)2+R1.98(1.10)3+R3.0203=R16.31老师帮忙看一下这样做有什么问题

NO.PZ201512300100001207问题如下7. Unr Scenario 1, the intrinsic value per share of the equity of Amersheen is closest to:A.R13.29.B.R15.57.C.R16.31.the multistage resiincome mol results in intrinsic value of R16.31.This variation of the multistage resiincome mol, in whiresiincome fas over time, is: where is the persistenfactor.The first step is to calculate resiincome per share for years 2012 2015:ROE = earnings / book valueGrowth rate = ROE × retention rateRetention rate = 1 (vin/earnings)Book valuet= book valuet 1 + earningst 1 vint 1Resiincome per share = EPS equity charge per shareEquity charge per share = book value per sharet× cost of equityUsing the resiincome per share for 2015 of R1.608, the seconstep is to calculate the present value of the terminvalue:PV of TerminValue =R1.6081+0.10-0.70(1.10)3=R3.0203Then, intrinsic value per share is:V0=R7.60+R2.52(1.10)+R2.31(1.10)2+R1.98(1.10)3+R3.0203=R16.31如图为什么不能这么算

NO.PZ201512300100001207 问题如下 7. Unr Scenario 1, the intrinsic value per share of the equity of Amersheen is closest to: A.R13.29. B.R15.57. C.R16.31. the multistage resiincome mol results in intrinsic value of R16.31.This variation of the multistage resiincome mol, in whiresiincome fas over time, is: where is the persistenfactor.The first step is to calculate resiincome per share for years 2012 2015:ROE = earnings / book valueGrowth rate = ROE × retention rateRetention rate = 1 (vin/earnings)Book valuet= book valuet 1 + earningst 1 vint 1Resiincome per share = EPS equity charge per shareEquity charge per share = book value per sharet× cost of equityUsing the resiincome per share for 2015 of R1.608, the seconstep is to calculate the present value of the terminvalue:PV of TerminValue =R1.6081+0.10-0.70(1.10)3=R3.0203Then, intrinsic value per share is:V0=R7.60+R2.52(1.10)+R2.31(1.10)2+R1.98(1.10)3+R3.0203=R16.31 1. T不是应该代表进入到第二段时间的时间吗?这道题的T难道不应该是2015吗?跟2016又有什么关系呀?2.我理解的是,下面黑色打印的这个公式T-1对应的就是2014年,用RI 2015计算对应2014年年底的PVRI然后折3年回去(也就是老师的红字部分),这个没问题。但是老师的解析我看写的“如果要使用李老师的公式,则需要向后推导一年,计算出RI2016以后才可以使用,并且折现的PVRI就会落在2015年年末,需要和2015年的RI=1.608一起折现4年到0时刻,就可以获得和本题一样的答案了”。这跟2016年有什么关系呢?如果2016年的话,不应该是RI(T+1)吗?既然是红色公式再向后一期推导出来的