F统计量怎么能看出来过度拟合的?为什么不是Adjust R2

问题如下图:

选项:

A.

B.

C.

解释:

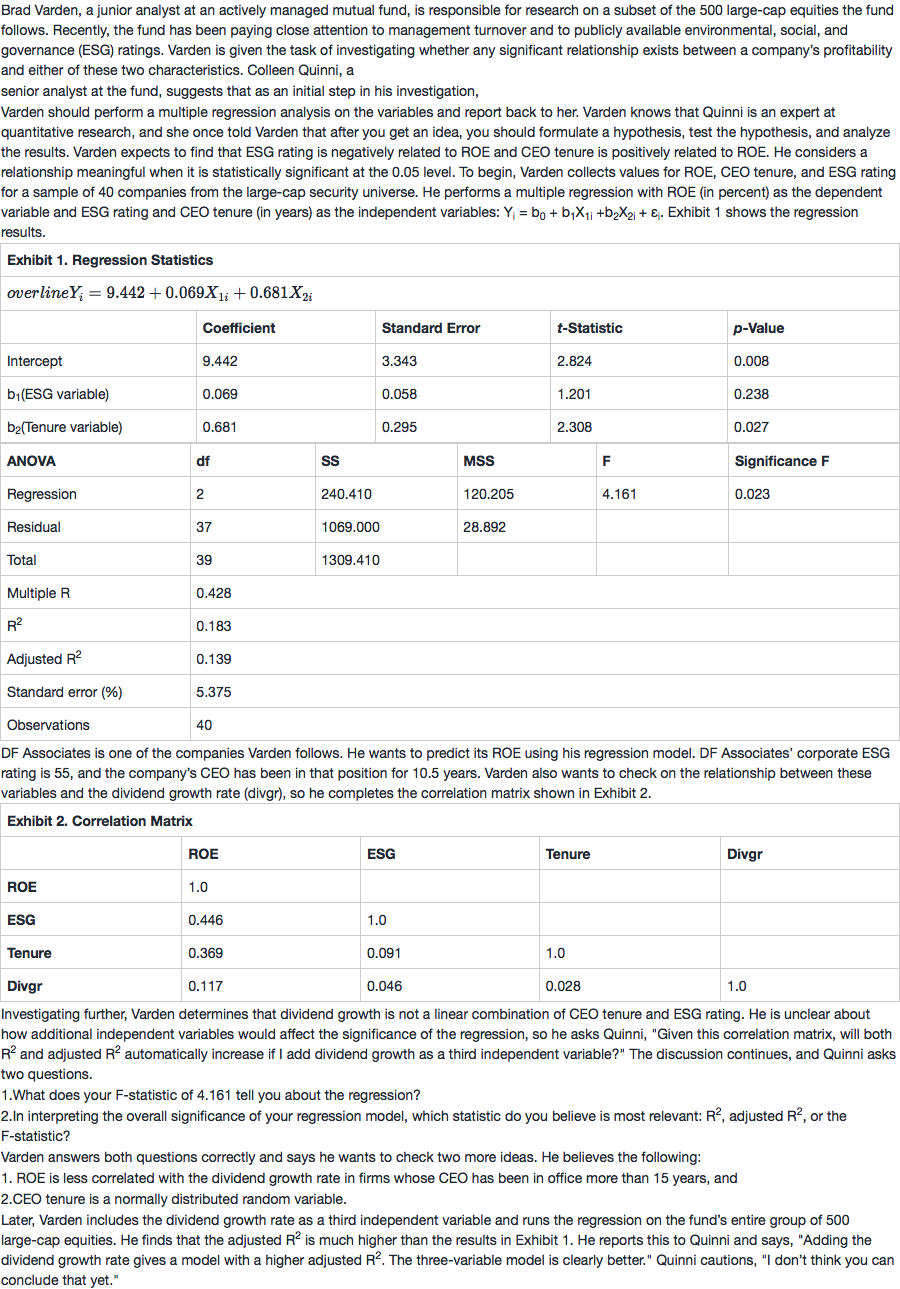

NO.PZ201709270100000307 7. Varn’s best answer to Quinni’s question about overall significanis: R2. austeR2. the F-statisti C is correct. In a multiple lineregression (comparewith simple regression), R2 is less appropriate a measure of whether a regression mol fits the ta well. A high austeR2 es not necessarily incate ththe regression is well specifiein the sense of inclung the correset of variables. The F-test is appropriate test of a regression’s overall significanin either simple or multiple regressions. 解析当中的这句话理解不了,麻烦老师给一下

7. Varn’s best answer to Quinni’s question about overall significanis: R2. austeR2. the F-statisti C is correct. In a multiple lineregression (comparewith simple regression), R2 is less appropriate a measure of whether a regression mol fits the ta well. A high austeR2 es not necessarily incate ththe regression is well specifiein the sense of inclung the correset of variables. The F-test is appropriate test of a regression’s overall significanin either simple or multiple regressions. 老师请问,对于显著性来说,R2是只针对一元回归?F statistic是针对多元回归?

没看明白,我选的B-_-||

这道题没太明白,austeR2不是所有inpennt variables能够多少的pennt variables么,为何不能说明整个回归方程的significance?