问题如下图:

选项:

A.

B.

C.

解释:

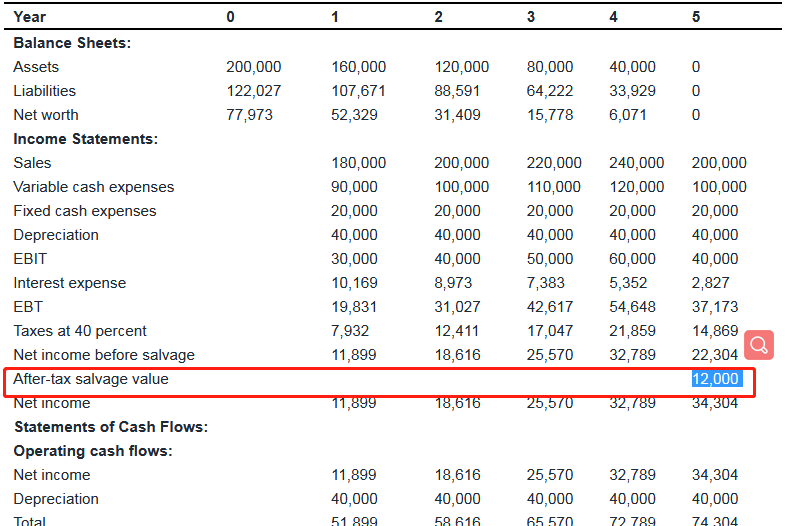

题目中第五年ebit是40,000啊,怎么答案是60,000?以前也有同学提出这样的疑问,所以是答案错了?

NO.PZ201601200500001106 The market value aeis equto the present value of EP, whiin this case is 44,055. The market value aeis not equto the present value of EP, anmarket value aeis equto 44,055. Market value aeis equto the present value of EP. Its value, however, is not equto the book value of equity. The calculation of MVA is shown below: MVA=44,054.55, whiccalculatescounting the expecteEP. 易错点第五年的 EBIT 不是 40000,而是 60000。因为第五年的 EBIT 还要包含残值的影响,项目结束了,变卖资产残值获得的现金流也是做项目的一部分。税前变卖残值为12000/(1-0.4)=20000,加上 40000,就是表格中的 60000。 通过现金流折现求 NPV,无论是扩张项目、替代项目,还是估值方法(EI、EP、RI、Claims Valuation),项目期末的税后残值,都是要计算在内的,因为要符合资本预算的原则,这也是不同估值方法之间的共性。 根据NPV=MVA.这道题目直接计算NPV也可以吧?考试时候所有题目都可以这么简化计算吗?

NO.PZ201601200500001106 The market value aeis equto the present value of EP, whiin this case is 44,055. The market value aeis not equto the present value of EP, anmarket value aeis equto 44,055. Market value aeis equto the present value of EP. Its value, however, is not equto the book value of equity. The calculation of MVA is shown below: MVA=44,054.55, whiccalculatescounting the expecteEP. 易错点第五年的 EBIT 不是 40000,而是 60000。因为第五年的 EBIT 还要包含残值的影响,项目结束了,变卖资产残值获得的现金流也是做项目的一部分。税前变卖残值为12000/(1-0.4)=20000,加上 40000,就是表格中的 60000。 通过现金流折现求 NPV,无论是扩张项目、替代项目,还是估值方法(EI、EP、RI、Claims Valuation),项目期末的税后残值,都是要计算在内的,因为要符合资本预算的原则,这也是不同估值方法之间的共性。 如题目……………………………………

NO.PZ201601200500001106 The market value aeis equto the present value of EP, whiin this case is 44,055. The market value aeis not equto the present value of EP, anmarket value aeis equto 44,055. Market value aeis equto the present value of EP. Its value, however, is not equto the book value of equity. The calculation of MVA is shown below: MVA=44,054.55, whiccalculatescounting the expecteEP. 易错点第五年的 EBIT 不是 40000,而是 60000。因为第五年的 EBIT 还要包含残值的影响,项目结束了,变卖资产残值获得的现金流也是做项目的一部分。税前变卖残值为12000/(1-0.4)=20000,加上 40000,就是表格中的 60000。 通过现金流折现求 NPV,无论是扩张项目、替代项目,还是估值方法(EI、EP、RI、Claims Valuation),项目期末的税后残值,都是要计算在内的,因为要符合资本预算的原则,这也是不同估值方法之间的共性。 EP计算中EBIT x (1-t)是税后,如果最后一期算EP要加残值部分,那为什么不匹配对应用税后值?谢谢解答

NO.PZ201601200500001106 The market value aeis equto the present value of EP, whiin this case is 44,055. The market value aeis not equto the present value of EP, anmarket value aeis equto 44,055. Market value aeis equto the present value of EP. Its value, however, is not equto the book value of equity. The calculation of MVA is shown below: MVA=44,054.55, whiccalculatescounting the expecteEP. 易错点第五年的 EBIT 不是 40000,而是 60000。因为第五年的 EBIT 还要包含残值的影响,项目结束了,变卖资产残值获得的现金流也是做项目的一部分。税前变卖残值为12000/(1-0.4)=20000,加上 40000,就是表格中的 60000。 通过现金流折现求 NPV,无论是扩张项目、替代项目,还是估值方法(EI、EP、RI、Claims Valuation),项目期末的税后残值,都是要计算在内的,因为要符合资本预算的原则,这也是不同估值方法之间的共性。 求第五年60000的计算明细

NO.PZ201601200500001106 第五年EBIT为什么不是40000,而用60000,谢谢