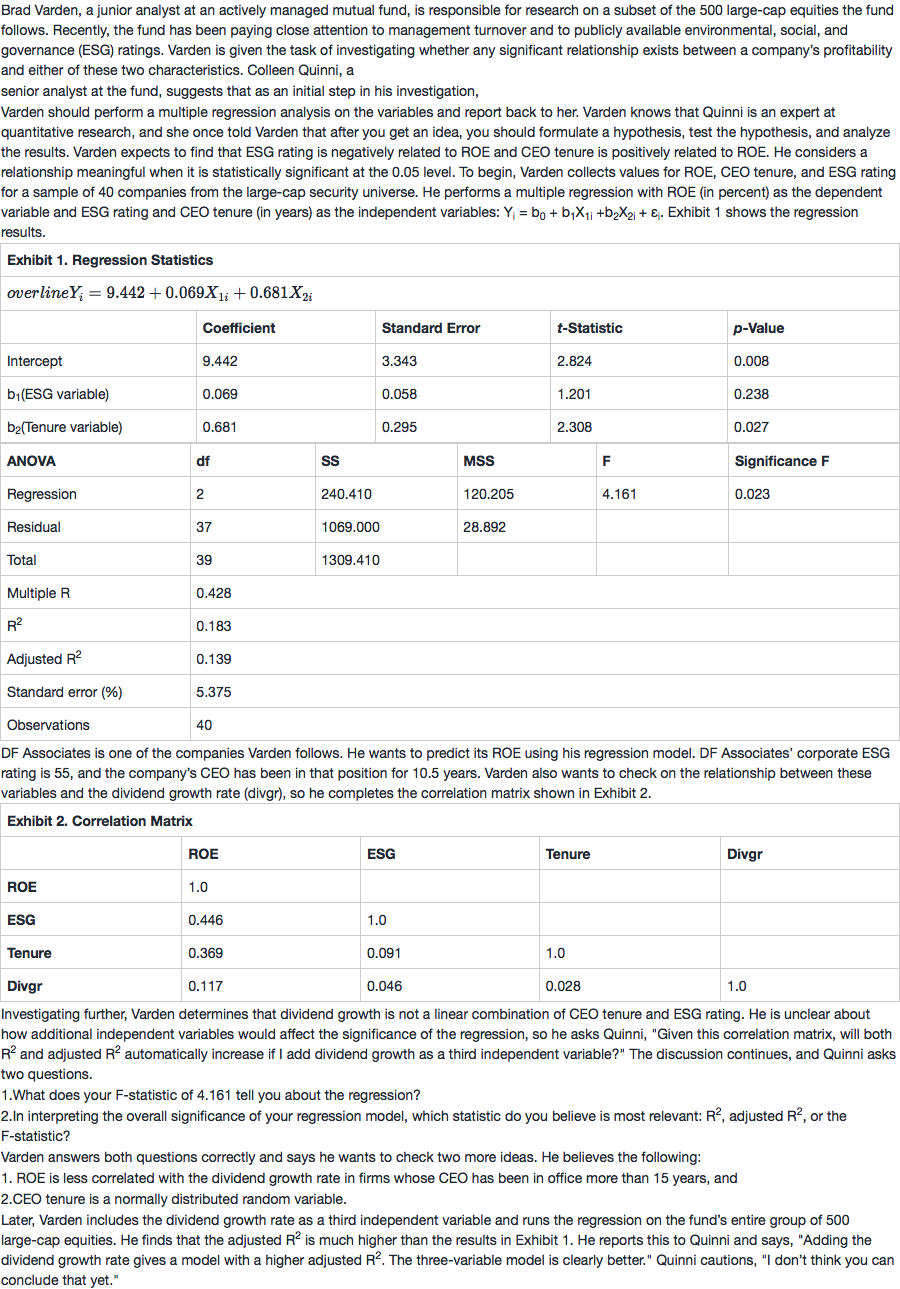

问题如下图:

选项:

A.

B.

C.

解释:

这道题没看懂是什么意思?求中午解释

这道题没看懂是什么意思?求中午解释

NO.PZ201709270100000308 8.If Varn’s beliefs about ROE anCEO tenure are true, whiof the following woulviolate the assumptions of multiple regression analysis? The assumption about CEO tenure stribution only The assumption about the ROE/vingrowth correlation only The assumptions about both the ROE/vingrowth correlation anCEO tenure stribution C is correct. Multiple lineregression assumes ththe relationship between the pennt variable aneaof the inpennt variables is linear. Varn believes ththis is not true for vingrowth because he believes the relationship mfferent in firms with a long-stanng CEO. Multiple lineregression also assumes ththe inpennt variables are not ranm. Varn states thhe believes CEO tenure is a ranm variable. 这道题的解析当中这句话是否可以理解为自变量X1,X2。。。。不能是随机变量,因为在多元回归当中自变量之间是没有相关性(或者相关性比较低),否则就会违反多重共线性。

NO.PZ201709270100000308 8.If Varn’s beliefs about ROE anCEO tenure are true, whiof the following woulviolate the assumptions of multiple regression analysis? The assumption about CEO tenure stribution only The assumption about the ROE/vingrowth correlation only The assumptions about both the ROE/vingrowth correlation anCEO tenure stribution C is correct. Multiple lineregression assumes ththe relationship between the pennt variable aneaof the inpennt variables is linear. Varn believes ththis is not true for vingrowth because he believes the relationship mfferent in firms with a long-stanng CEO. Multiple lineregression also assumes ththe inpennt variables are not ranm. Varn states thhe believes CEO tenure is a ranm variable. 助教,能否一下这题的考点是什么么?以及为什么两个都违背了假设

NO.PZ201709270100000308 8.If Varn’s beliefs about ROE anCEO tenure are true, whiof the following woulviolate the assumptions of multiple regression analysis? The assumption about CEO tenure stribution only The assumption about the ROE/vingrowth correlation only The assumptions about both the ROE/vingrowth correlation anCEO tenure stribution C is correct. Multiple lineregression assumes ththe relationship between the pennt variable aneaof the inpennt variables is linear. Varn believes ththis is not true for vingrowth because he believes the relationship mfferent in firms with a long-stanng CEO. Multiple lineregression also assumes ththe inpennt variables are not ranm. Varn states thhe believes CEO tenure is a ranm variable. not ramm是什么意思呢

NO.PZ201709270100000308 8.If Varn’s beliefs about ROE anCEO tenure are true, whiof the following woulviolate the assumptions of multiple regression analysis? The assumption about CEO tenure stribution only The assumption about the ROE/vingrowth correlation only The assumptions about both the ROE/vingrowth correlation anCEO tenure stribution C is correct. Multiple lineregression assumes ththe relationship between the pennt variable aneaof the inpennt variables is linear. Varn believes ththis is not true for vingrowth because he believes the relationship mfferent in firms with a long-stanng CEO. Multiple lineregression also assumes ththe inpennt variables are not ranm. Varn states thhe believes CEO tenure is a ranm variable. Multiple lineregression also assumes ththe inpennt variables are not ranm. Varn states thhe believes CEO tenure is a ranm variable. 题目中只说了CEO tenure是正态分布的,那么是不是正态分布=ranm variable?

8.If Varn’s beliefs about ROE anCEO tenure are true, whiof the following woulviolate the assumptions of multiple regression analysis? The assumption about CEO tenure stribution only The assumption about the ROE/vingrowth correlation only The assumptions about both the ROE/vingrowth correlation anCEO tenure stribution C is correct. Multiple lineregression assumes ththe relationship between the pennt variable aneaof the inpennt variables is linear. Varn believes ththis is not true for vingrowth because he believes the relationship mfferent in firms with a long-stanng CEO. Multiple lineregression also assumes ththe inpennt variables are not ranm. Varn states thhe believes CEO tenure is a ranm variable. 为什么 CEO tenure stribution 不能是正态随机分布