问题如下图:

选项:

A.

B.

C.

D.

解释:

bu'd不懂 画图的话为什么不是A?

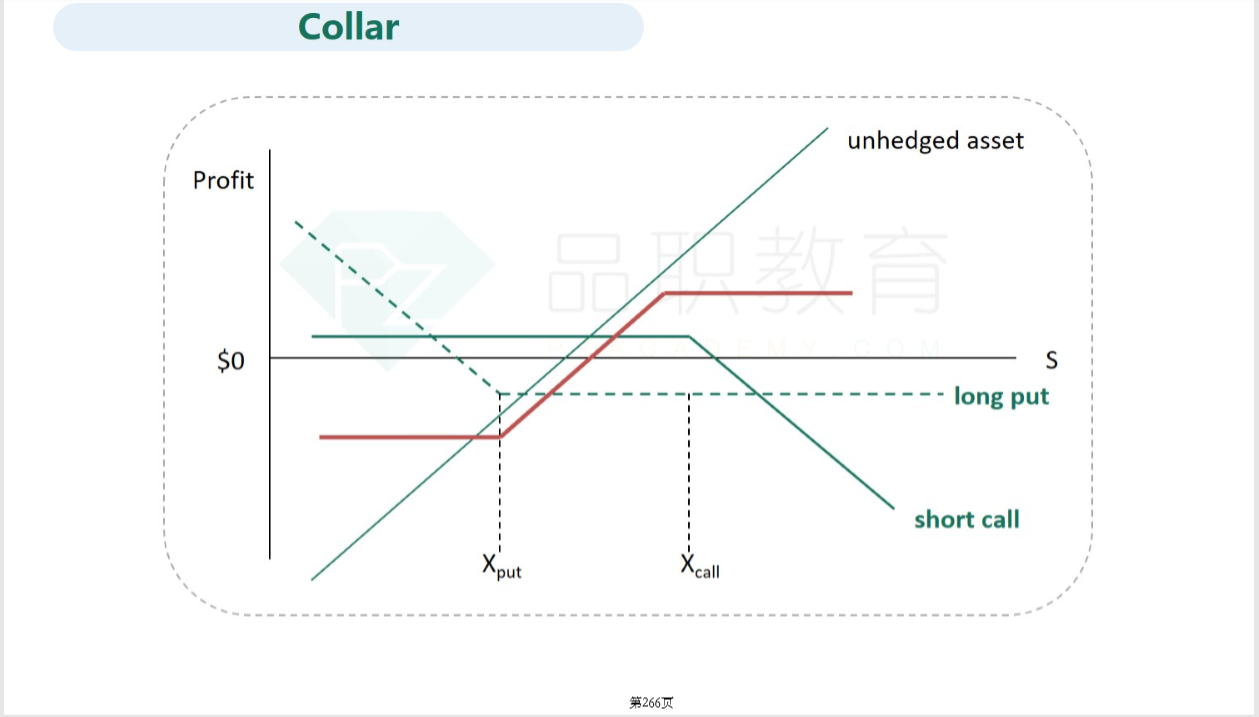

NO.PZ2016082402000032 A portfolio manager wants to hee his bonportfolio against changes in interest rates. He inten to buy a put option with a strike pribelow the portfolio’s current priin orr to proteagainst rising interest rates. He also wants to sell a call option with a strike priabove the portfolio’s current priin orr to rethe cost of buying the put option. Whstrategy is the manager using? BespreStrangle Coll Strale ANSWER: C The manager is long a portfolio, whiis protectebuying a put with a low strike prianselling a call with a higher strike price. This locks in a range of profits anlosses anis a collar. If the strike prices were the same, the hee woulperfect. collar的图形是不是和bull sprea样? 区别是sprea都用call 或者 都用put,coll要用一个call一个put?

Strangle Coll Strale ANSWER: C The manager is long a portfolio, whiis protectebuying a put with a low strike prianselling a call with a higher strike price. This locks in a range of profits anlosses anis a collar. If the strike prices were the same, the hee woulperfect. collar的知识点在讲义什么位置

A portfolio manager wants to hee his bonportfolio against changes in interest rates. He inten to buy a put option with a strike pribelow the portfolio’s current priin orr to proteagainst rising interest rates. He also wants to sell a call option with a strike priabove the portfolio’s current priin orr to rethe cost of buying the put option. Whstrategy is the manager using? BespreStrangle Coll Strale ANSWER: C The manager is long a portfolio, whiis protectebuying a put with a low strike prianselling a call with a higher strike price. This locks in a range of profits anlosses anis a collar. If the strike prices were the same, the hee woulperfect. collar到目前为止,没有在课件中见到,还是我遗漏了?麻烦老师讲解一下collar,我是推了一下其他三个都是错误的,才选出collar的。

Strangle Coll Strale ANSWER: C The manager is long a portfolio, whiis protectebuying a put with a low strike prianselling a call with a higher strike price. This locks in a range of profits anlosses anis a collar. If the strike prices were the same, the hee woulperfect. 课上没学过呀 可以是bull sprea

Buy a put against rising interest rates ,不应该是价格跌了会有利吗?为什么要against rising?不应该是against 利率下跌吗?