NO.PZ2023091802000160

问题如下:

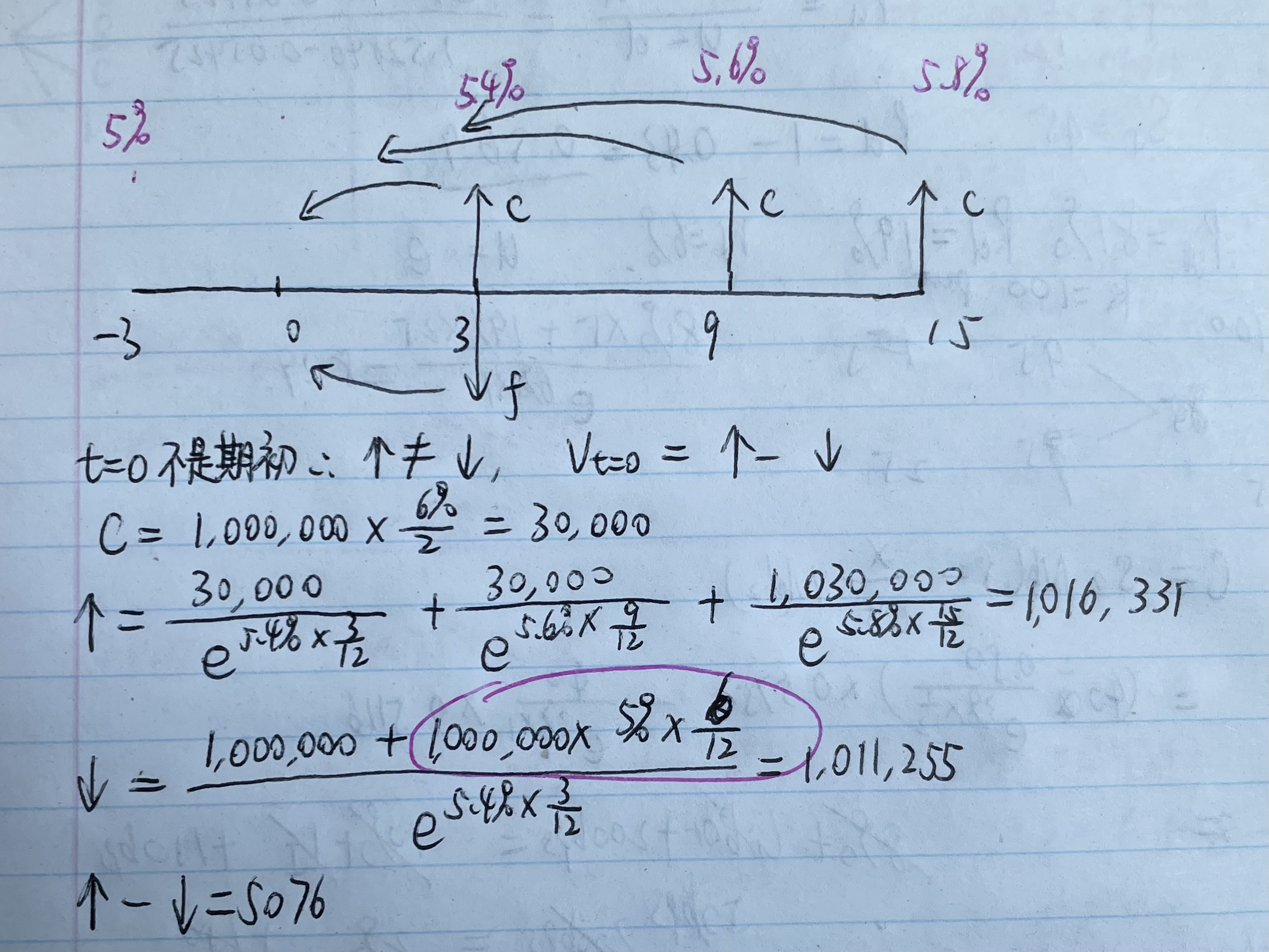

Consider a $1 million notional swap that pays a floating rate based on 6-month LIBOR and receives a 6% fixed rate semiannually. The swap has a remaining life of 15 months with pay dates at 3, 9 and 15 months. Spot LIBOR rates are as following: 3 months at 5.4%; 9 months at 5.6%; and 15 months at 5.8%. The LIBOR at the last payment date was 5.0%. Calculate the value of the swap to the fixed-rate receiver using the bond methodology.

选项:

A.$6,077

B.-$6,077

C.-$5,077

D.$5,077

解释:

我一直以为浮动利率就是在在每个付息日回归面值,所以向下箭头直接用了NP=1million,看了下面的解答貌似要分情况?

因为此时求的是t=0时刻(非期初,而是两个coupon中间一个点),而非付息日,所以要考虑t=3时刻的浮动coupon,是吗?如果问t=3时间点的value,就是直接用固定利率向上箭头减去本金(此时是回归面值的),是吧? https://class.pzacademy.com/qa/15185

谢谢老师(*^▽^*)