NO.PZ2023101902000020

问题如下:

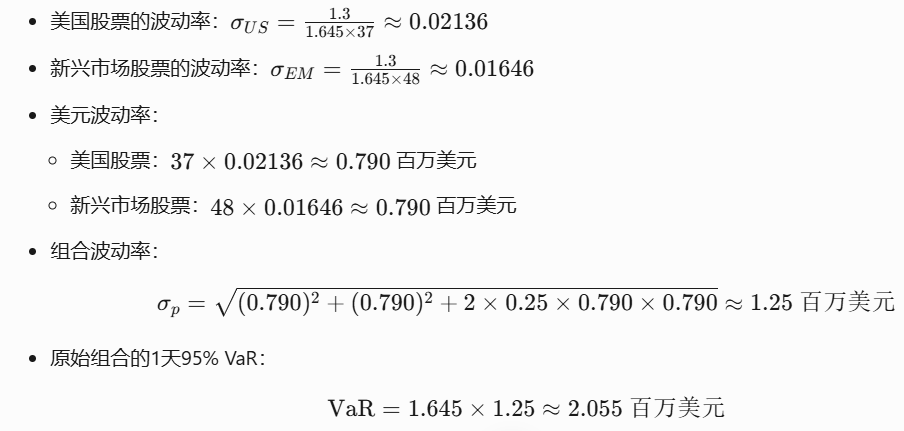

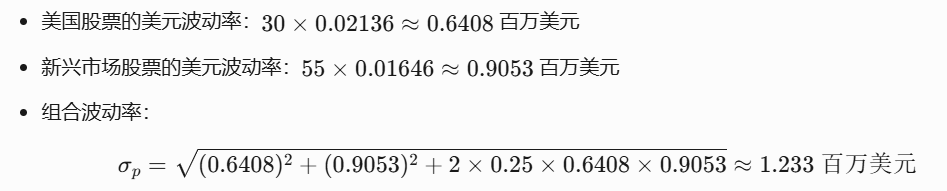

A wealth management firm has a portfolio consisting of USD 37 million invested in US equities and USD 48 million invested in emerging markets equities. The US equities and emerging markets equities both have a 1-day 95% VaR of USD 1.3 million. The correlation between the returns of the US equities and emerging markets equities is 0.25. While rebalancing the portfolio, the manager in charge decides to sell USD 7 million of the US equities to buy USD 7 million of the emerging markets equities. At the same time, the CRO of the firm advises the portfolio manager to change the risk measure from 1-day 95% VaR to 10-day 99% VaR. Assuming that returns are normally distributed and that the rebalancing does not affect the volatility of the individual equity positions, by how much will the portfolio VaR increase due to the combined effect of portfolio rebalancing and change in risk measure?选项:

A.USD 4.373 million

B.USD 6.428 million

C.USD 7.034 million

D.USD 9.089 million

这道题能给个计算过程吗