NO.PZ2018123101000107

问题如下:

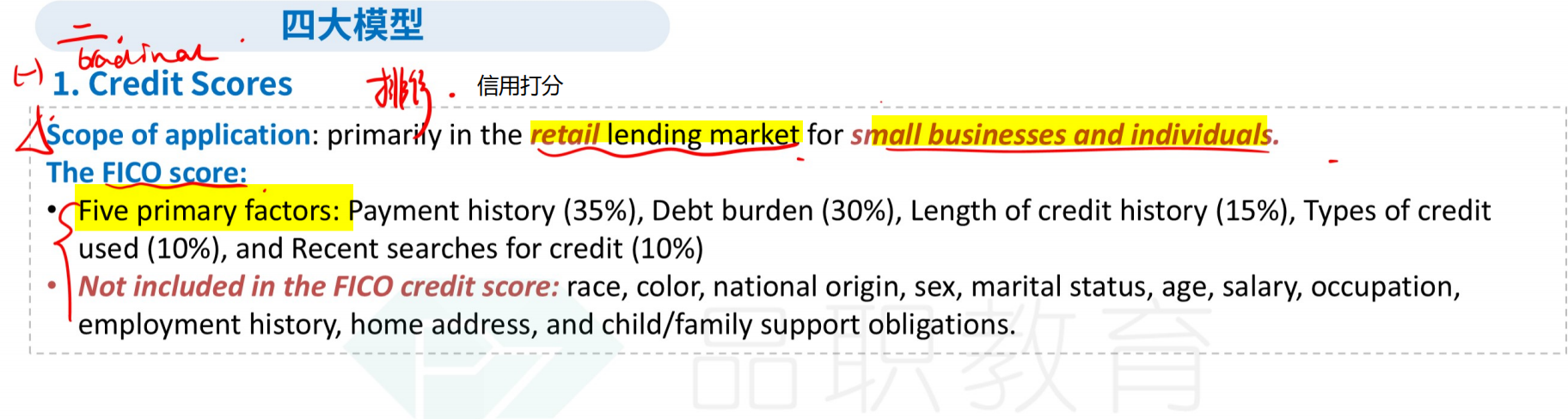

Cromwell works with another analyst, George Hastings, to discuss credit scoring and credit rating models. Hastings starts the conversation by saying, “Credit scoring models are primarily applied to consumers or small business borrowers. In some cases, only negative information, such as delinquencies or defaults, are used, while other models use a mix of factors, such as payment history and recent credit searches.” The focus of credit scores is the probability of default. Hastings continues, “Credit ratings, on the other hand, are used in the corporate and sovereign bond market and also for asset-backed securities. Ratings are focused on probability of default. Credit rating agencies, such as Standard & Poor’s, consider the loss given default by means of notching, which adjusts the issue rating to reflect the priority of claims in the capital structure."

Are Hastings’s comments regarding credit scores and credit ratings most likely correct?

选项:

A.Yes

B.No, he is incorrect with regard to credit scores.

C.No, he is incorrect with regard to credit ratings.

解释:

Hastings’s comments regarding both credit scores and

credit ratings are correct.

强化班这里说credit score模型里面的FICO就包含了recent searches for credit and payment history

请问为什么我们还认为他的观点正确呢??