NO.PZ2018122701000081

问题如下:

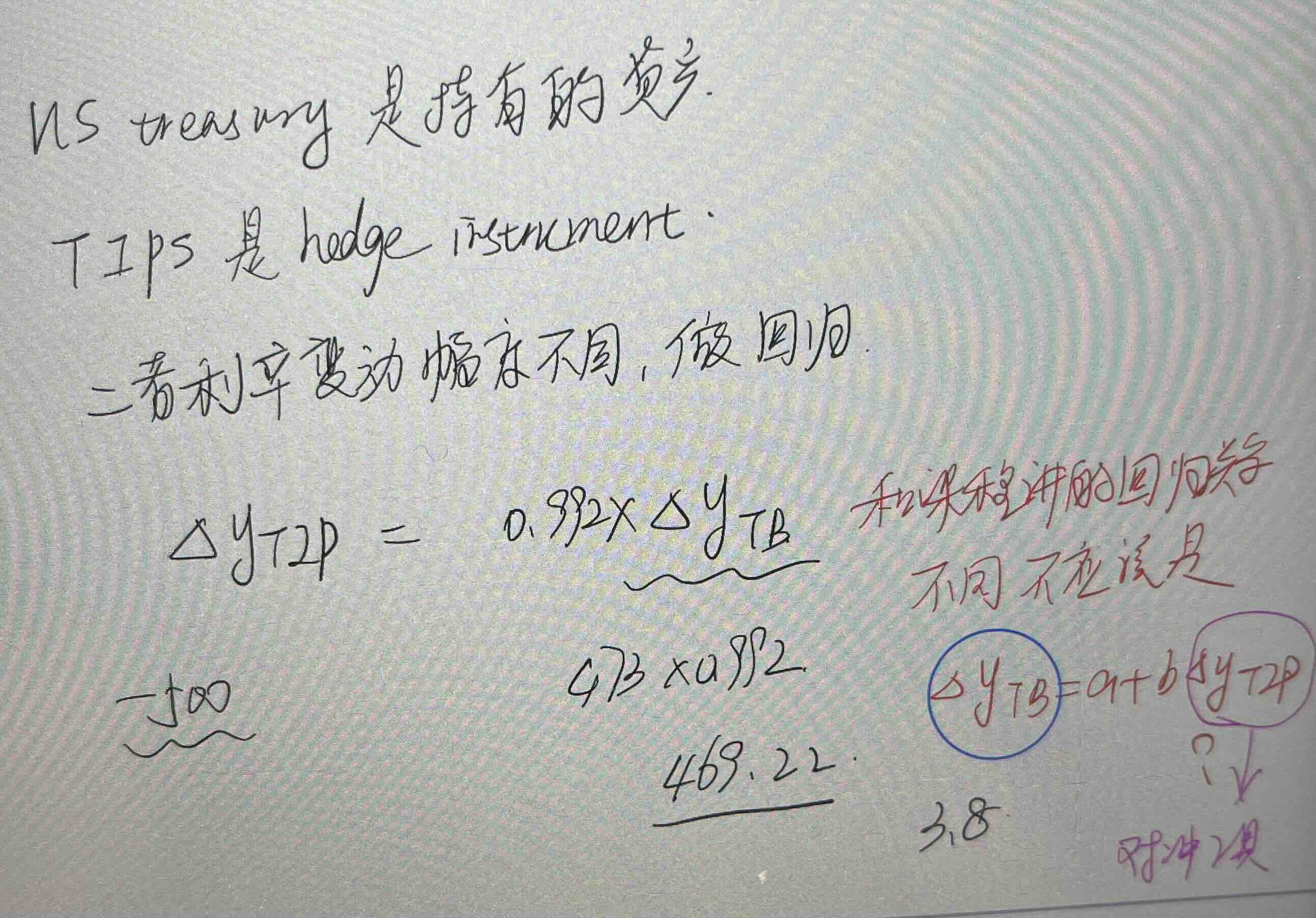

The trading department of Dragon Fruit Bank now has a hedging position based on the duration. They shorted the $ 500 million U.S. Treasury bond and bought the $ 473 million U.S. TIPS. The analysis department of the bank has just made a regression analysis of the nominal interest rate and real interest rate, and found that when the nominal interest rate changes by 1 basis point, the real interest rate changes by 0.992 basis points. Based on this relationship, how should the trading department adjust their existing positions?

选项:

A.

There is no need to change the position.

B.

purchase $3.8 million TIPS.

C.

Purchase $4.8 million Treasury bond

D.

Sell $3.8 million TIPS

解释:

B is correct.

考点:Empirical Approaches To Risk Metrics And Hedging

解析:因为利率变化不同,原有的duration hedge平衡被打破了,实际需要的TIPS是473/0.992=476.8 million。所以要再买3.8million的TIPS。

老师好,虽然做对了,但是感觉和课程里讲的回归的谁是X,谁是Y不同,哪里想错了吗?