NO.PZ201701230200000605

问题如下:

5. If Deem Advisors enters into a new offsetting contract two months after purchasing protection on Kand Corporation, this action will most likely result in:

选项:

A.a loss on the CDS position.

B.a profit on the CDS position.

C.neither a loss or a profit on the CDS position.

解释:

B is correct.

Deem Advisors purchased protection and therefore is economically short and benefits from an increase in the company’s spread. Since putting on the protection, the credit spread increased by 200 bps, and Deem Advisors realizes the profit by entering into a new, offsetting contract (sells protection to another party at a higher premium).

A is incorrect because a decrease (not increase) in the spread would result in a loss for the credit protection buyer. C is incorrect because Deem Advisors, the credit protection buyer, would profit from an increase in the company’s credit spread, not break even.

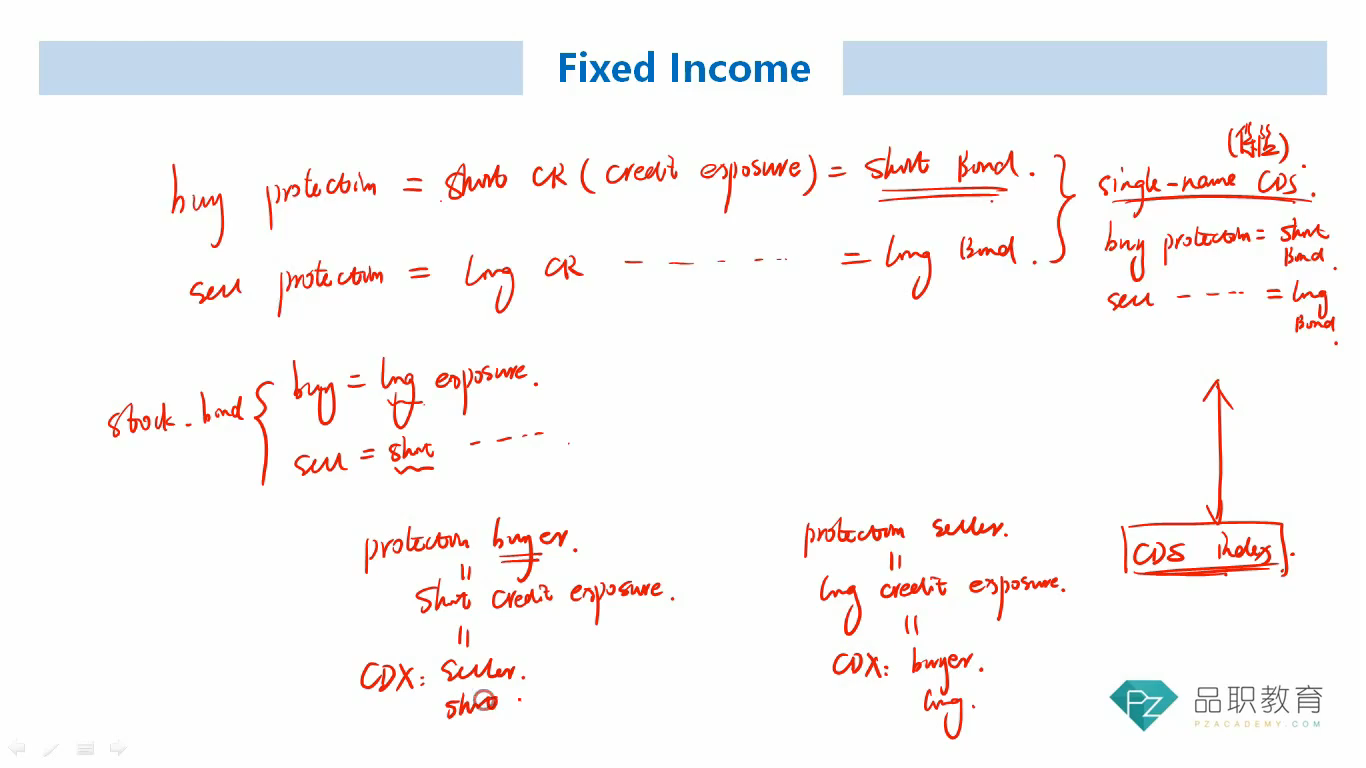

buy CDS=sell protection

sell CDS=buy protection