NO.PZ202308140300008204

问题如下:

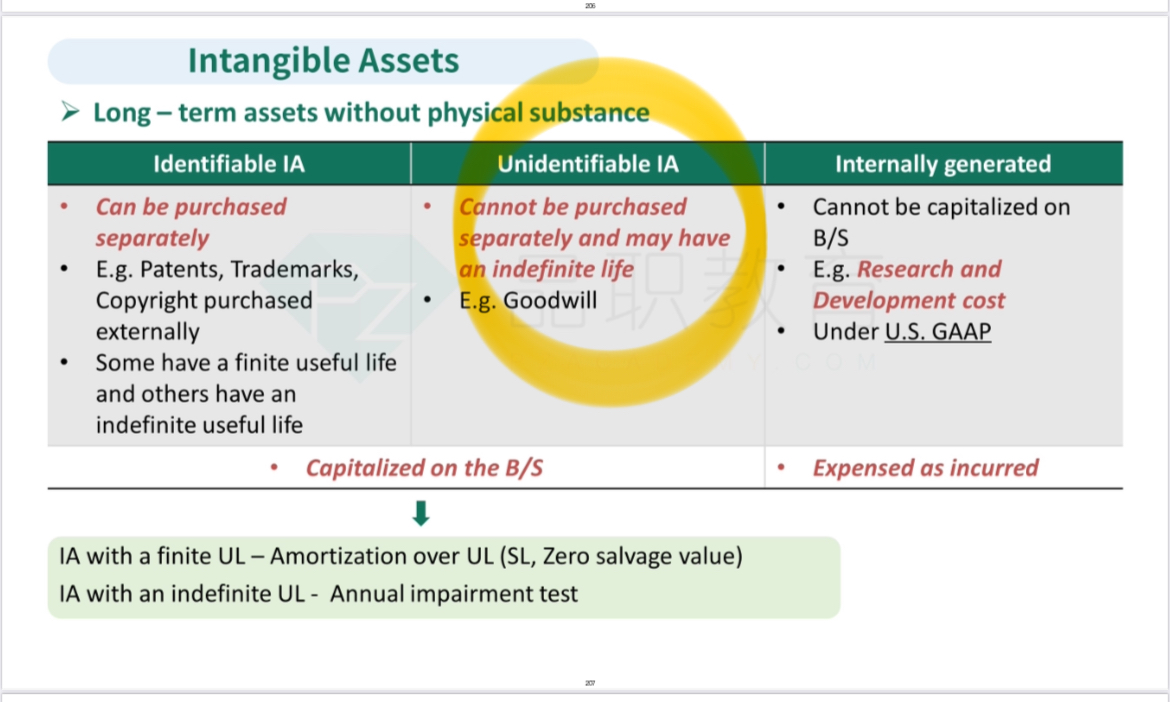

Q. Under US GAAP, when assets are acquired in a business combination, goodwill most likely arises from:

选项:

A.contractual or legal rights.

B.assets that can be separated from the acquired company.

C.assets that are neither tangible nor identifiable intangible assets.

解释:

C is correct. Under both IFRS and US GAAP, if an item is acquired in a business combination and cannot be recognized as a tangible asset or identifiable intangible asset, it is recognized as goodwill. Under US GAAP, assets arising from contractual or legal rights and assets that can be separated from the acquired company are recognized separately from goodwill.

请详解一下知识点以及对应的讲义的位置