NO.PZ2024102501000011

问题如下:

Rob Smith, as portfolio manager at Pell Tech University Foundation, is respon sible for the university’s USD3.5 billion endowment. The endowment supports the majority of funding for the university’s operating budget and financial aid programs, and it is invested in fixed income, public equities, private equities, and real assets.

The Pell Tech Board is conducting its quarterly strategic asset allocation review. T he board members note that although performance has been satisfactory, they have two concerns:

1. Endowment returns have underperformed in comparison to those of univer sity endowments of similar size.

2. Return expectations have shifted lower for fixed-income and public equity investments.

Smith attributes this underperformance to a lower risk profile relative to that of its peers because of a lower allocation to illiquid private equity investments. In response to the board’s concerns, Smith proposes an increase in the allocation to the private equity asset class. His proposal uses option price theory for valuation purposes and is supported by Monte Carlo simulations.

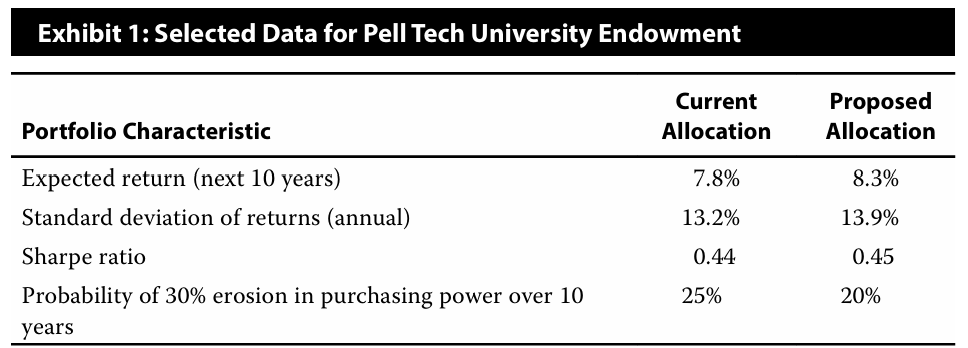

Exhibit 1 presents selected data on the current university endowment.

Discuss two reasons the increased risk profile is appropriate. Justify your response.

选项:

解释:

Reasons to justify the increased risk profile include the following:

a. The board members’ lower return expectations for public equity and f ixed-income asset classes imply that a higher level of risk must be taken to achieve the same level of returns.

b. For a long-horizon institutional investor such as Pell Tech, the ability to tol erate illiquidity creates an opportunity to improve portfolio diversification and expected returns as well as access a broader set of investment strategies. In mean–variance optimization models, the inclusion of illiquid assets in the eligible investment universe might shift the efficient frontier for the portfo lio upward, theoretically resulting in greater efficiency (i.e., higher expected returns will be gained across all given levels of risk).

c. T he portfolio risk profile for the endowment is currently more conservative in comparison to that of peer universities.

d. Smith’s Monte Carlo simulations suggest that the proposed asset allocation has a higher probability of achieving the return target while better preserv ing the purchasing power of the endowment.

The sharpe ratio of proposed allocation is higher than current allocation.The expected return increases rapidly than the standard deviation of rururns. What's more, the probability of 30% erosion in purcashing power over 10 years is lower in proposed allocation than current allocation.

麻烦老师提供一个准确且简化的答题模板,谢谢