NO.PZ2024102501000010

问题如下:

Rob Smith, as portfolio manager at Pell Tech University Foundation, is respon sible for the university’s USD3.5 billion endowment. The endowment supports the majority of funding for the university’s operating budget and financial aid programs, and it is invested in fixed income, public equities, private equities, and real assets.

The Pell Tech Board is conducting its quarterly strategic asset allocation review. T he board members note that although performance has been satisfactory, they have two concerns:

1. Endowment returns have underperformed in comparison to those of univer sity endowments of similar size.

2. Return expectations have shifted lower for fixed-income and public equity investments.

Smith attributes this underperformance to a lower risk profile relative to that of its peers because of a lower allocation to illiquid private equity investments. In response to the board’s concerns, Smith proposes an increase in the allocation to the private equity asset class. His proposal uses option price theory for valuation purposes and is supported by Monte Carlo simulations.

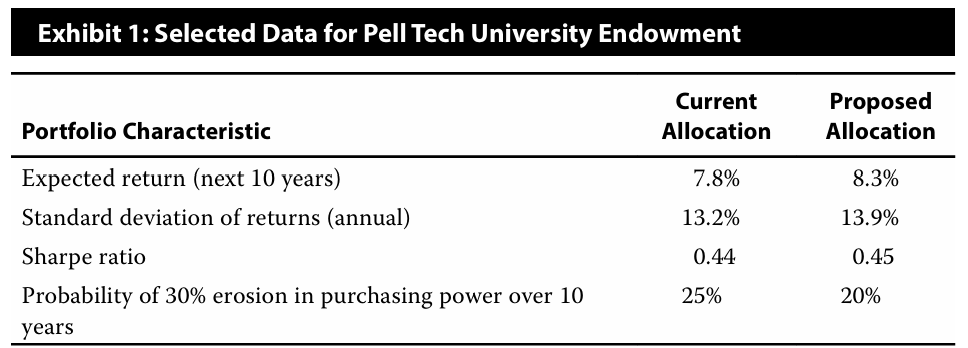

Exhibit 1 presents selected data on the current university endowment.

Discuss Smith’s method for estimating the increase in return expectations derived from increasing the endowment allocation to private equity.

选项:

解释:

Private equity is recognized as an illiquid alternative investment and could offer higher returns via a liquidity premium.

The illiquidity premium (also called the liquidity premium) is the expected compensation for the additional risk of tying up capital for a potentially uncertain time period. It can be estimated, as Smith has done, by using the idea that the size of a discount an investor should receive for such capital commitment is rep resented by the value of a put option with an exercise price equal to the hypothet ical “marketable price” of the illiquid asset as estimated at the time of purchase. Smith can derive the price of the illiquid private equity asset by subtracting the put price from the “marketable price.” If both the “marketable price” and the illiquid asset price are estimated or known, then the expected return for each can be calculated, with the difference in expected returns representing the illiquidity premium (in %).

Smith 通过期权价格理论来估计流动性溢价,进而预估增加私募股权投资配置所带来的回报增长。他认为投资者在购买私募股权这种非流动性资产时,所应获得的折扣(即流动性溢价)可以用一个看跌期权的价值来表示,该看跌期权的行权价格等于购买时估计的非流动性资产的假设 “可销售价格”。通过从 “可销售价格” 中减去看跌期权价格,Smith 可以得到私募股权资产的价格,从而计算出其预期回报。与其他流动性较好的资产预期回报相比,两者的差值即为流动性溢价,这部分溢价即为增加私募股权投资配置所带来的额外回报预期增长的一部分

PE投资liquiding premium,这个是不是就是short put,类似我为了收 liquidity premium(放弃权利),类比callable bond,只不过是short call变成short 普通,谢谢

何老师上课有讲,所以这里面opinion theory是这个,谢谢。