NO.PZ202001110100001303

问题如下:

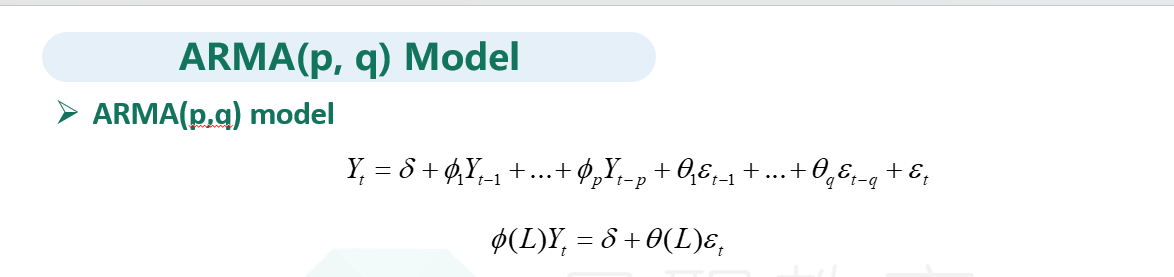

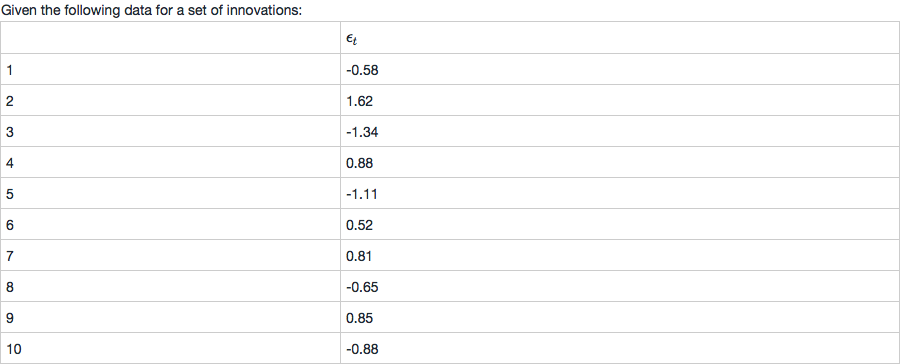

c. Calculate the time series for the following ARMA(1,1) model, taking

选项:

解释:

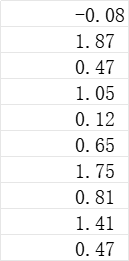

Each value is generated via the formula:

q1 = 0.5 + 0.375 * 0 + 0.375 * 0 - 0.58 = -0.08

z2 = 0.5 + 0.375(-0.08) + 0.375(-0.58) + 1.62 = 1.87

and so forth.

我算出来是