NO.PZ2024082801000075

问题如下:

Alwyn Rivera Case Scenario

Alwyn Rivera is a portfolio manager at Elite Investments (EI) based in the US. Rivera has a shortlist of 50 US public firms and wants to better understand the factors that may explain the cross-sectional variation in these stocks' returns. Based on the finance literature, Rivera believes that firm size and book-to-market ratio are important factors that need to be included in his model. He also thinks that being included in the Dow Jones Industrial Average Index (DJIA) can help a firm get more media attention and potentially attract more investors, which in turn may affect a stock's return.

To test his theory, Rivera collects the annual returns (r) of these 50 stocks in the year that just ended, as well as their market capitalizations (in billions of dollars) and book-to-market ratios (BMRatio) at the end of the previous year. He also creates a dummy variable (InDow) that is coded 1 if a stock is included in the DJIA and 0 otherwise, and then runs the following regression:

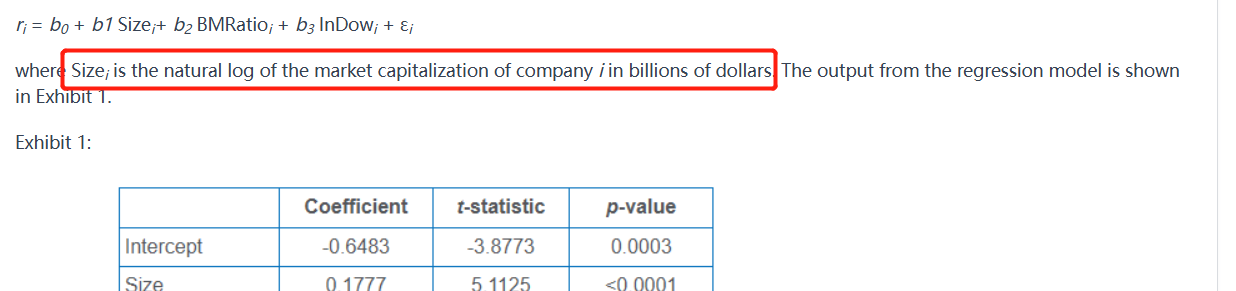

ri = b0 + b1 Sizei+ b2 BMRatioi + b3 InDowi + εi

where Sizei is the natural log of the market capitalization of company i in billions of dollars. The output from the regression model is shown in Exhibit 1.

Exhibit 1:

Rivera shows his model and results to a summer intern, and asks whether he should use the reported R2 or adjusted R2 to measure the goodness of fit of his model. The intern replies, "Adjusted R2 would be more appropriate in this case because the model has more than one independent variable. Adjusted R2 is adjusted for degrees of freedom and nondecreasing in the number of independent variables."

The predicted annual return for a stock that is included in the DJIA, has a market capitalization of $52 billion and a book-to-market ratio of 0.45 is closest to:

选项:

A.A.– 9.08%.

B.B.3.59%.

C.C.7.33%.

解释:

A is Correct because the estimated model is Ri = –0.6483 + 0.1777 × Sizei + 0.0433 × BMRatioi – 0.1641 × InDowi. When Sizei = ln(52), BMRatioi = 0.45, and InDowi = 1, the predicted return would be – 0.6483 + 0.1777 × ln(52) + 0.0433 × 0.45 – 0.1641 × 1 ≈ – 0.0908 = –9.08%.

B is Incorrect because this is the result when the dollar amount of the market capitalization is plugged into the estimated model, instead of using the amount expressed in billions of dollars. Further, the answer is incorrectly adjusted to a percentage. The estimated model is Ri = –0.6483 + 0.1777 × Sizei+ 0.0433 × BMRatioi – 0.1641 × InDowi. When Sizei = ln(52,000,000,000), BMRatioi = 0.45, and InDowi = 1, the expected return would be –0.6483 + 0.1777 × ln(52000000000)i + 0.0433 × 0.45 – 0.1641 × 1 ≈ 3.59, adding a % sign to get 3.59%.

C is Incorrect because this is the expected return for a stock that not in the DJIA. with a market capitalization of $52 billion and a book-to-market ratio of 0.45. The estimated model is Ri = –0.6483 + 0.1777 × Sizei+ 0.0433 × BMRatioi – 0.1641 × InDowi. When Sizei = ln(52), BMRatioi = 0.45, and InDowi = 0, the predicted return would be – 0.6483 + 0.1777 × ln(52) + 0.0433 × 0.45 – 0.1641 × 0 ≈ 0.0733 = 7.33%.

请问size为啥是Ln52,公式里不是52吗