NO.PZ2024062801000053

问题如下:

A bank has the major part of its assets in 30-year fixed-rate mortgages. The bank has a small amount of core deposits but is mostly funded with repurchase agreements and negotiable certificates of deposit (CDs). Assuming the bank’s assets are approximately 10% greater than its liabilities, the bank’s leverage-adjusted duration gap is most likely:

选项:

A.

positive.

B.

negative.

C.

zero.

D.

equal to its duration gap.

解释:

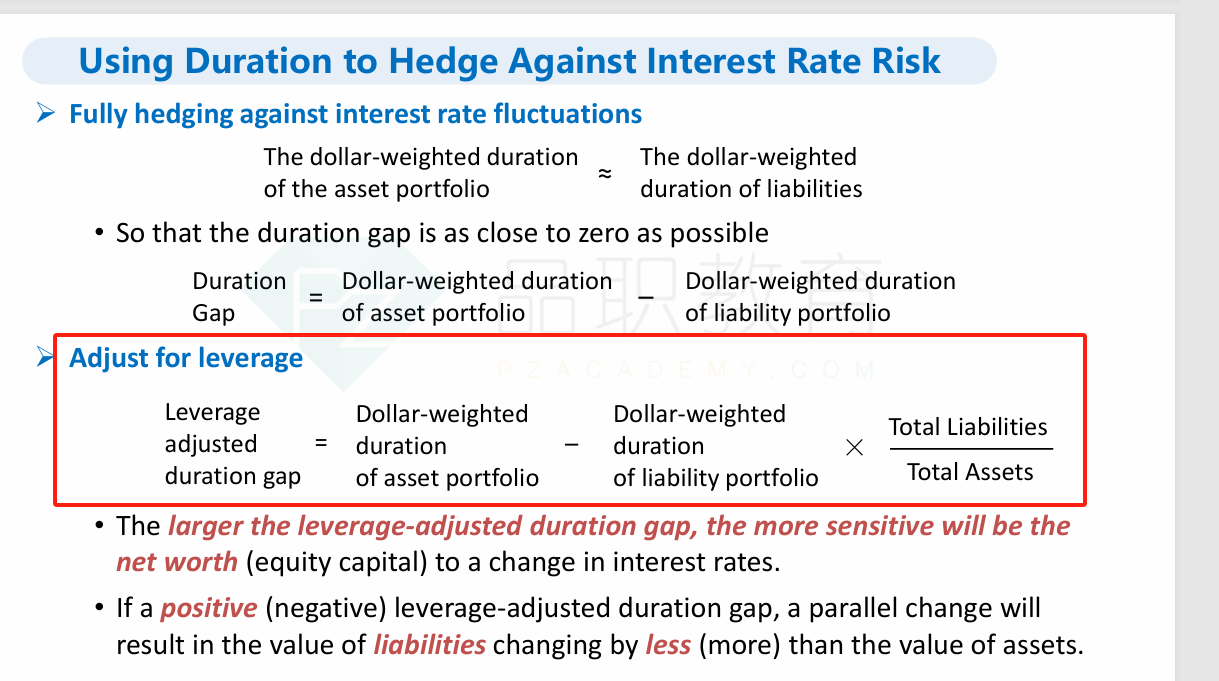

鉴于其资产和负债的平均期限之间存在较大差异,经杠杆调整后的久期缺口将是正数。这家银行的资产期限较长(久期较长),而其负债期限较短(久期较短)。这意味着银行的久期缺口将是正的,而其利率敏感性缺口(IS Gap)可能为负(在收益率曲线呈正斜率的情况下)。简而言之,银行的资产比负债对利率变化更为敏感,长期资产占比大,短期负债占比大,这在利率上升时可能对其盈利造成不利影响。

老师好,leverage adjusted duration gap是啥意思?是和课件里interest sensitive gap是一个意思吗?