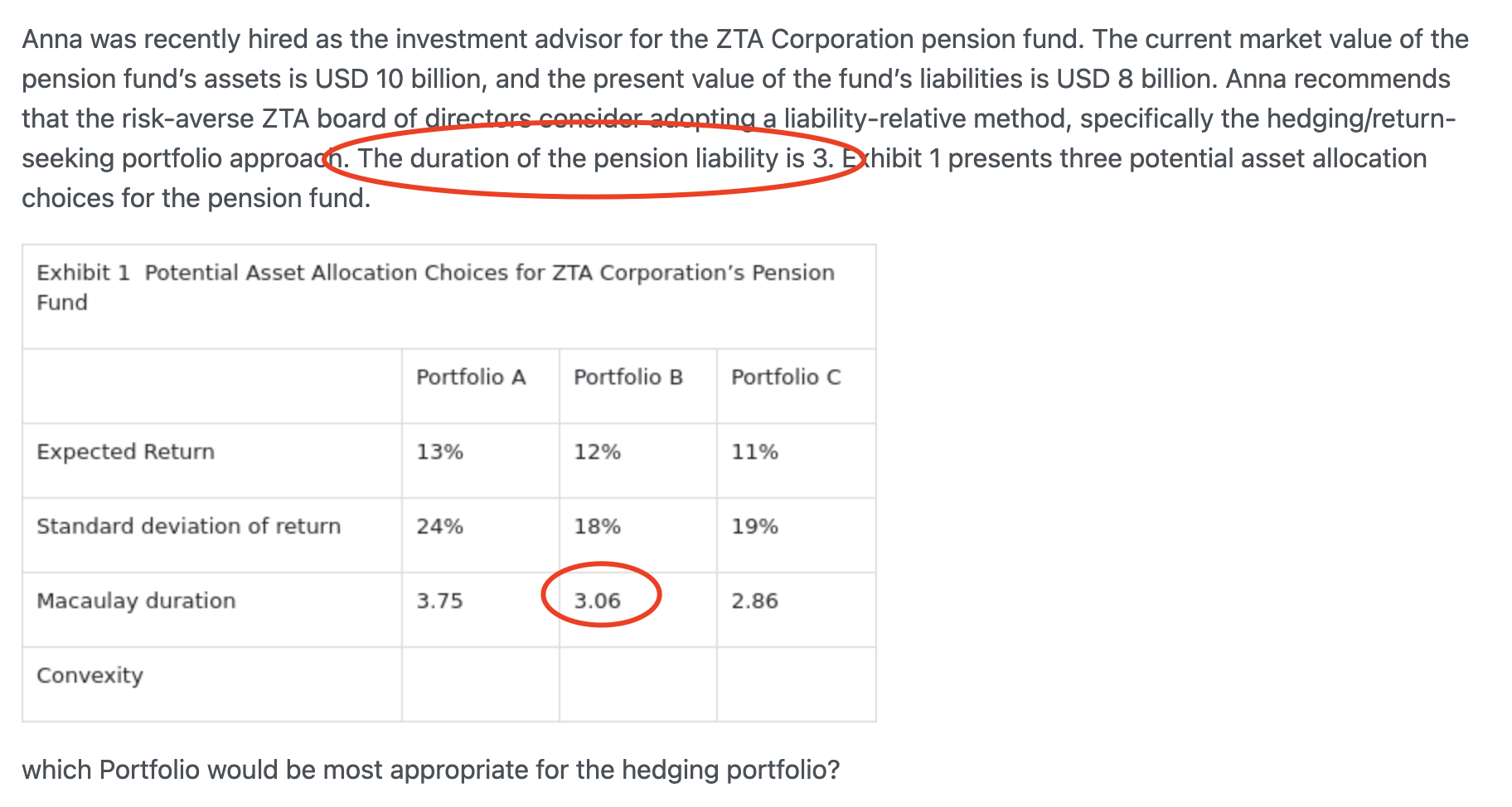

The hedging portfolio must include assets whose returns are driven by the same factors that drive the returns of the liabilities.

这里我想到另一道题,是主观题也是hedging return seeking,里面liability是inflation-linked,所以asset也要用inflation-linked去match liability

这两题结合一起我想问“assets whose returns are driven by the same factors that drive the returns of the liabilities.”这句话是不是就是immunization的本质,就是MacD或者BPV closely match?还是说这个same factors有额外需要了解的东西?