NO.PZ2016031001000119

问题如下:

Which of the following statements about duration is correct?

选项:

A.A bond’s coupon rate and duration are positively related.

B.A bond’s duration is inversely related to its yield-to-maturity.

C.The Macaulay duration of a zero-coupon bond is less than its time-to-maturity.

解释:

B is correct.

A bond’s yield-to-maturity is inversely related to its duration: The higher the yield-to-maturity, the lower its duration and the lower the interest rate risk.

A bond’s coupon rate is inversely related to its duration. Zero-coupon bonds do not pay periodic coupon payments; therefore, the Macaulay duration of a zero-coupon bond is its time-to-maturity.

考点:Properties of Duration

解析:coupon rate越大,代表期间现金流越多,也就是前期的现金流较多,还款更快,duration越小,呈反向关系,故A选项不正确。

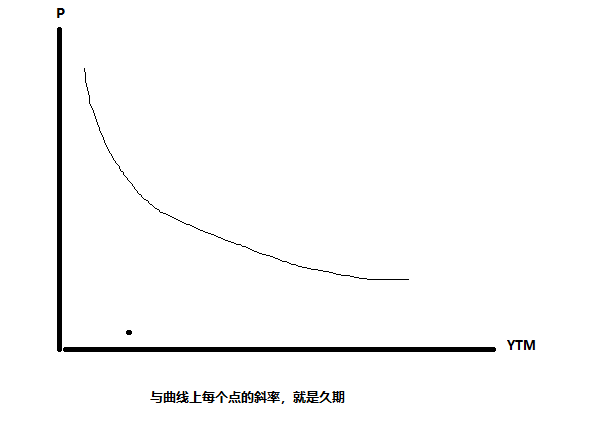

YTM和duration的变化情况,可以从斜率或一阶导出发去考虑。折现率越大,斜率的绝对值越小(duration代表斜率的绝对值),所以利率越大,duration越小。两者是反向关系。故选项B正确。

Macaulay duration衡量的是现金流的平均还款期(现金流到账时间),而零息债券只有一笔现金流,所以其macaulay duration就等于它的time-to-maturity,故选项C不正确。

YTM和duration的变化情况,可以从斜率或一阶导出发去考虑。折现率越大,斜率的绝对值越小(duration代表斜率的绝对值),所以利率越大,duration越小。两者是反向关系。

YTM和duration的关系能不能用其他的理解角度再解释一下,不是很能理解这个斜率一阶导的角度