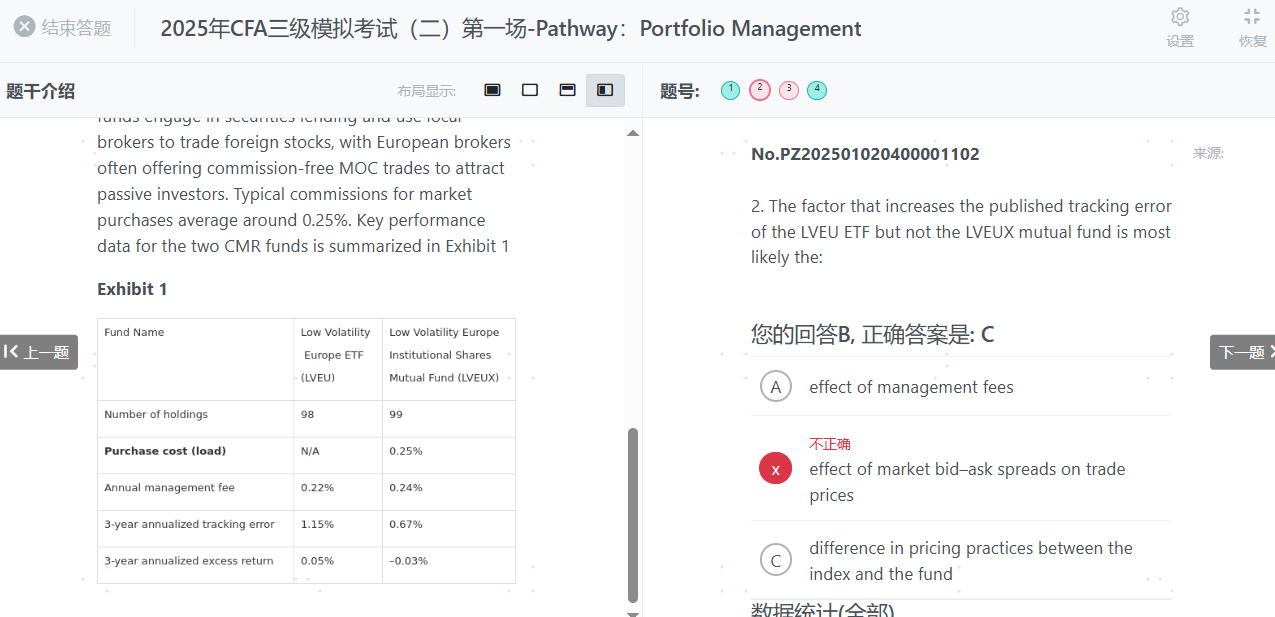

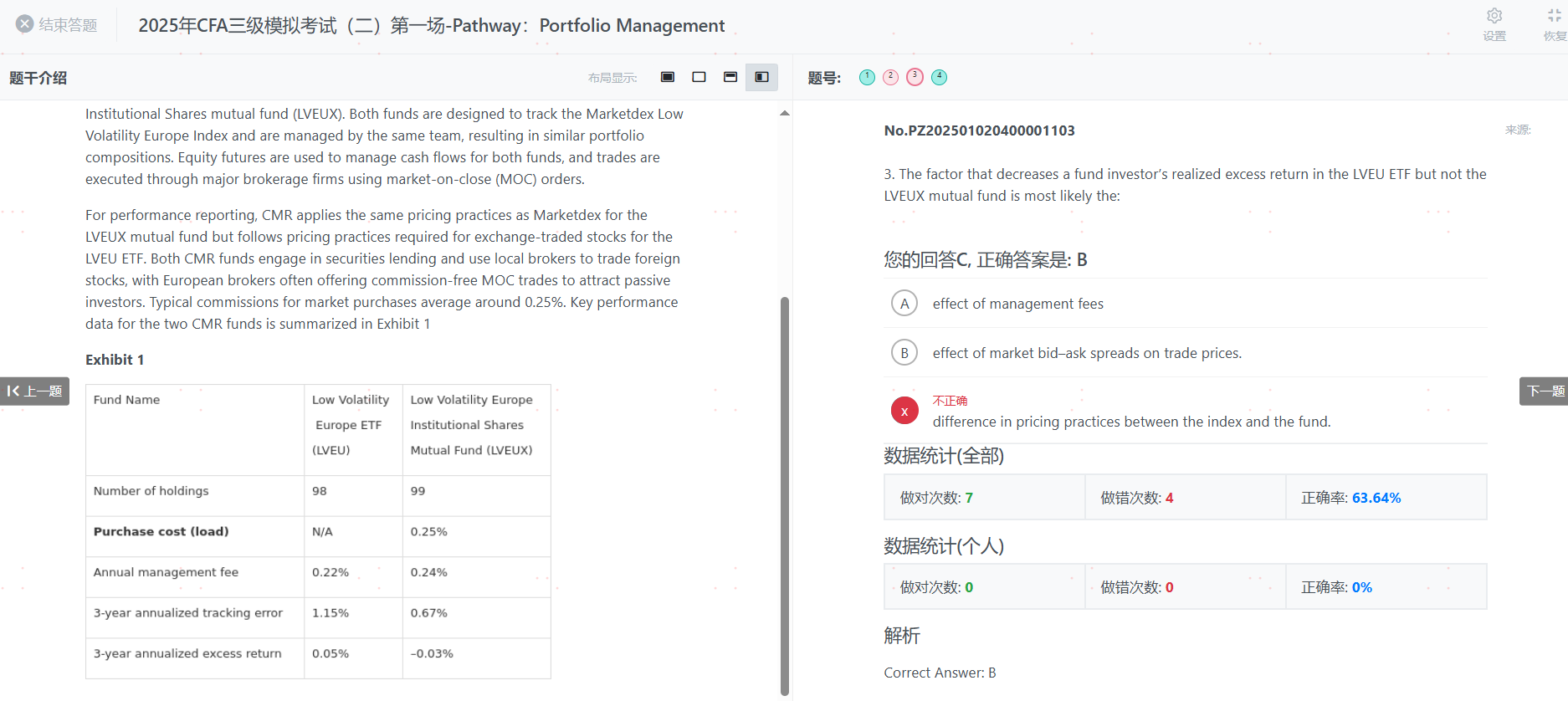

这两道题辛苦结合在一起讲一下effect of market bid–ask spreads on trade prices、difference in pricing practices between the index and the fund分别对 ETF和mutual fund的tracking error、realized excess return影响

第一道题关于tracking error影响,答案说mutual fund和index都受到bid-ask spread影响,而ETF不受到bid-ask spread影响,既然如此,那ETF因为不受到bid-ask spread影响,反而会增加tracking error啊,因为指数benchmark会受到影响,只是正偏离,为啥不选C

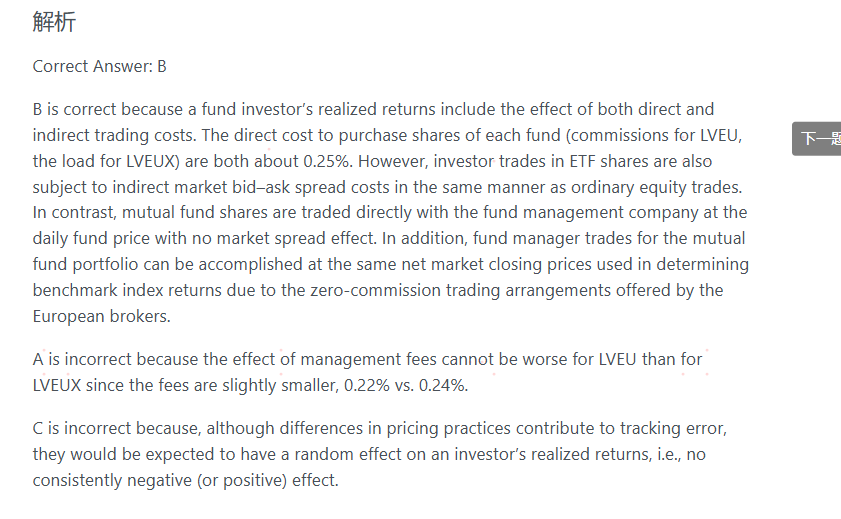

第二道题对于bid-ask spread的影响答案的解析反而和第一道题相反,答案说ETF又会受到bid-ask spread影响,这不是自相矛盾吗?

另外第一道题算tracking error时,用的是ETF net asset value return和benchmark return的trading error(一级市场);但是第二道题算excess return,却用的是ETF 的trading price return(二级市场),这也太双标了吧

这里的第几题。

这里的第几题。