NO.PZ2023071902000006

问题如下:

Question

An investor reviews the rate quotes for the Brazilian real (BRL) and the

Australian dollar (AUD) and decides to short BRL520,000.

Spot rate BRL/AUD: 2.1150

BRL 1-year interest rate: 4.3%

Forward rate BRL/AUD: 2.1410

AUD 1-year interest rate: 3.3%

选项:

A.–BRL6,500.B.BRL1,400. C.BRL6,580.

解释:

Solution

-

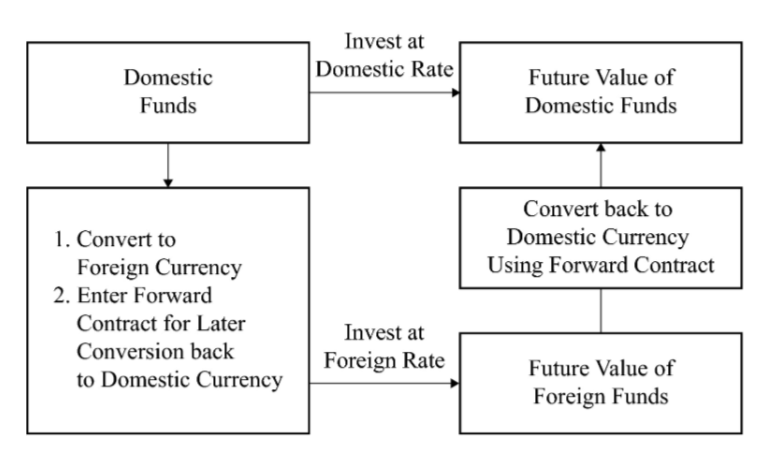

Correct. The equation below represents the "covered interest arbitrage relationship." If this relationship is not satisfied, a risk-free arbitrage opportunity exists.

(1+id)=Sf/d(1+if)(1Ff/d)

Left Side of Equation: BRL520,000 × (1 + 0.043) = BRL542,360

Right Side of Equation:

Step Transaction Explanation

1 BRL520,000 × (1/2.1150AUD/BRL) = AUD245,862.88 Convert domestic to foreign

2 AUD245,862.88 × (1.033) = AUD253,976.36 Invest foreign at foreign rate

3 AUD253,976.36 × 2.1410 = BRL543,763.39 Convert foreign to domestic

Arbitrage profit = BRL543,763.39 – BRL542,360 ≈ BRL1,403

• explain the arbitrage relationship between spot and forward exchange rates and interest rates, calculate a forward rate using points or in percentage terms, and interpret a forward discount or premium

等式左侧:BRL520,000 × (1 + 0.043) = BRL542,360

等式左边:BRL520,000 × (1 + 0.043) = BRL542,360

等式右边:

步骤交易说明:

1 BRL520,000 × (1/2.1150 aud /BRL) = AUD245,862.88,即用本币兑换外币

2 AUD245,862.88 × (1.033) = AUD253,976.36,即按外国汇率进行海外投资

3 AUD253,976.36 × 2.1410 = BRL543,763.39,即外币兑换国内货币

套利利润= BRL543,763.39 - BRL542,360≈BRL1,403

左边是F/S, 右边是(1+BRL)/(1+AUD),这样算为什么不对?