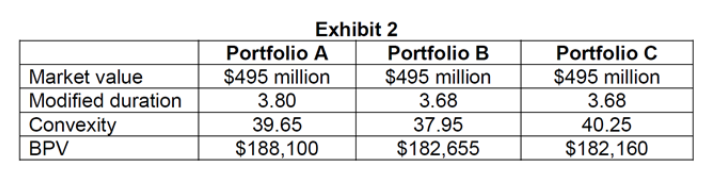

这个题为什么要用duration match 多负债,选组合C?多负债不是应该用BPVmatch,然后让convexity大于负债的,在此基础上越小越好吗?我认为应该是选组合A,从Market value 和BPV 角度不能排除,最后从convexity 角度就可以把B和C排除:

Portfolio A would best immunize Endicott’s debt liabilities.

to immunize the debe liabilities:

1.the market value of asset should euqal or exceed the PV of the liabilities.(the all three portfolios are meet the reuqirement)

2.the BPV of the assets should closely match the liabilities.(the all three portfolios are meet the reuqirement)

3.and,the convexity of the assets should larger than the liabilities conveixty,and as low as possible.the portfolio A has a convexity of 39.6 is larger than liabilities convexity 39.5,and just a little more .