这道题就是考查Forward rate bias的理解。关于汇率与利率的关系,我们学过2个interest rate parity。

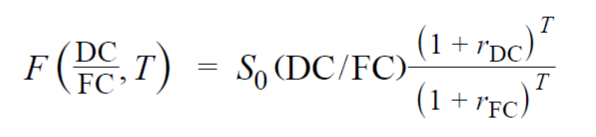

一个是covered interest rate parity。这个利率平价一定成立,因为他是forward外汇远期合约的定价机制。这个利率平价就是给foward合约定价F的:

这里面说,如果本国利率rDC更高,国外利率rFC更低,则Forward合约里面锁的的汇率是:高利率国家汇率贬值,低利率国家汇率相对升值。

汇率的升贬值完全就等于两国的利息差,汇率升贬值会抹平息差。

所以,在两个国家投资,且用foward合约锁定换汇汇率,则换成同一个货币之后,两国的投资收益率是一样大的。

这个covered interest parity是一定成立的,因为里面存在着强约束关系,就是我们可以用forward合约,两国利率进行套利。如果不成立,强约束套利会推动着这层关系成立。

还有一个利率平价,是uncovered interest rate parity。

他是说,从长期来看,利率高的国家汇率贬值,利率低的国家汇率升值。最终,汇率的升贬值恰好抹平了两国息差,考虑汇率升贬值之后,两国的投资收益率换成统一货币后,应该是一样大的。天下大同。

可以发现,uncovered interest rate parity与covered interest rate parity的理念是一样的,都是低利率国家货币升值,高利率国家货币贬值,且升贬值幅度恰好抹平息差。

但区别是,CIRP里面涉及的汇率是forward合约锁定的汇率。covered interest rate parity一定成立,有forward合约的套利保障他一定成立。

而uncovered interest rate parity不一定成立,因为没有forward合约的强套利机制,只有从长期来看,才会趋向于成立。UCIRP里面涉及的汇率是预期的未来市场汇率。

所以,如果UCIRP与CIRP同时成立,那么代表的是UCIRP预期的未来市场汇率,就等于CIRP里面forward合约锁定的汇率。

如果UCIRP不成立时,forward合约里面锁定的汇率就不等于预期的未来市场汇率。这种不相等,就是forward rate bias。

题目说,如果存在forward rate bias,其实是告诉我们,UCIRP不成立。那我们就可以借入低利率,投资高利率,来赚取两国的息差。因为此时汇率波动不会抹平息差。我们做carry trade是有可能赚到息差收益的。这是做carry trade的一个理论前提:UCIRP不成立,汇率波动不会抹平两国息差。

选项A:

Investors tend to favor fixed-income investments in currencies that trade at a premium on a forward basis.

这里面的currencies that trade at a premium on a forward basis是说,forward合约里面锁定的汇率,比当前的市场即期汇率更高,forward rate存在premium。

在forward合约里,利率低的货币forward会升值,存在forward premium。所以这句话实际是想说,这个货币是低利率国家的国家。

我们应该是借入低利率国家货币,而选项A却说:favor fixed-income investments在这个货币上,选项A是说应该投资这个低利率货币。

这个说法错误。

选项B:

Investors tend to hedge fixed-income investments in higher-yielding currencies given the potential for lower returns due to currency depreciation.

选项B说,投资高利率国家时,应该要进行hedge,因为该国的货币会贬值。

在利用UCIRP进行carry trade时,是不会进行hedge的。

如果使用forward进行hedge的话,是无法赚到息差的,因为使用forward就涉及到了CIRP,forward合约锁定的汇率波动会抹平息差。最终赚到的收益率为0.

所以选项B其实就不是UCIRP的应用。

选项C:

Investors tend to favor unhedged fixed-income investments in higher-yielding currencies that are sometimes enhanced by borrowing in lower-yielding currencies.

这里说,投资者会borrow lower-yield currencies,借入低利率,同时投资higher-yield currencies投资高利率,并且不hedge(unhedge)。

这点完全正确。在UCIRP不成立时,就是借入低利率,投资高利率赚取息差。并且不会进行hedge。所以本题选C

这道题其实就是要从forward rate bias推出uncovered interest rate parity不成立,然后知道在这种条件下,carry trade是盈利的策略。所以要借低利率,投资高零零赚息差。而且carry trade不会进行hedge。