问题如下:

Pete Aron, portfolio manager for Gulf & Co.’s European technology fund, is concerned about currency fluctuations related to the equity portfolio (the Portfolio). The Portfolio is valued in USD, but has exposure to multiple European currencies, primarily the EUR.

Aron formulates the following market expectations for the coming year:

- Expected return (in EUR) of the Portfolio: +13.2%

- Standard deviation (in EUR) of the Portfolio: 15%

- Expected USD/EUR spot rate in one year: 1.2045 (1 EUR = 1.2045 USD)

- Standard deviation of the USD/EUR exchange rate: 5%

- Correlation between the USD/EUR exchange rate and the Portfolio (in EUR): –0.07

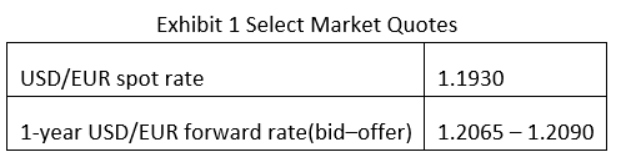

The market quotes presented in Exhibit 1 are available from a currency dealer:

Aron considers selling EUR and buying USD using a one-year forward contract to fully hedge the EUR currency risk. He will execute the trade if he can achieve the following risk/return objectives:

Objective 1: Increase the Portfolio’s expected return (in USD) by at least 25 basis points.

Objective 2: Reduce the Portfolio’s expected standard deviation (in USD) by at least 30 basis points.

Determine, based on Aron’s market expectations, whether he should execute the forward trade with respect to each of the following:

i. Objective 1

ii. Objective 2

Justify your response. Show your calculations. (2015 Q9)

对于利用forward contract to hedge的时候用bid还是ofr 的价格还是有些弄不清楚逻辑,就这道题来说,我的想法是 目前持有的是USD资产,担心USD贬值,所以需要short USD 或者long EUR,题目中给的标的是EUR,所以要用long 的头寸,就是需要从中介手里买,那对应的就是高的价格1.2090,请问这样思考的问题在哪里?正确的思路是如何?谢谢