NO.PZ2024120401000017

问题如下:

In running a regression of the returns of Stock XYZ against the returns on the market, the standard deviation of the returns of Stock XYZ is 20%, and that of the market returns is 15%. What is the maximum possible value of beta given that the standard deviation of the returns of Stock XYZ is 20% and those of the market is 15%?

选项:

A.

0.75

B.

1.0

C.

1.33

D.

1.50

解释:

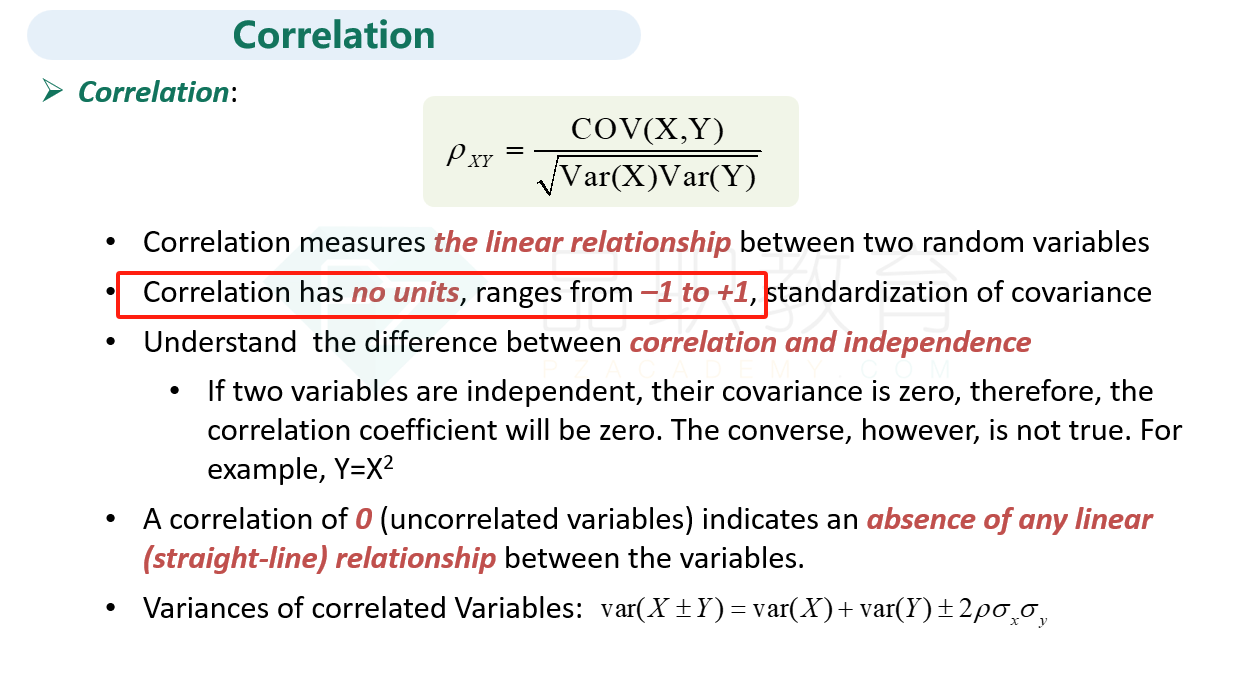

The maximum correlation is 1, therefore:

为什么max correlation为1 线性的correlation不是正无穷到负无穷吗