NO.PZ201803130100000602

问题如下:

Construct the overall goals-based asset allocation for the Armstrongs given their three goals and Abbott’s suggestion for investing any excess capital. Show your calculations.

Show your calculations.

选项:

解释:

Guideline Answer:

■ The module that should be selected for each goal is the one that offers the highest return given the time horizon and required probability of success.

■ Approximately 16.4%, 12.7%, 50.4%, and 20.5% should be invested in Modules A, B, C, and D, respectively. The appropriate goals-based allocation for the Armstrongs is as follows:

Supporting calculations:

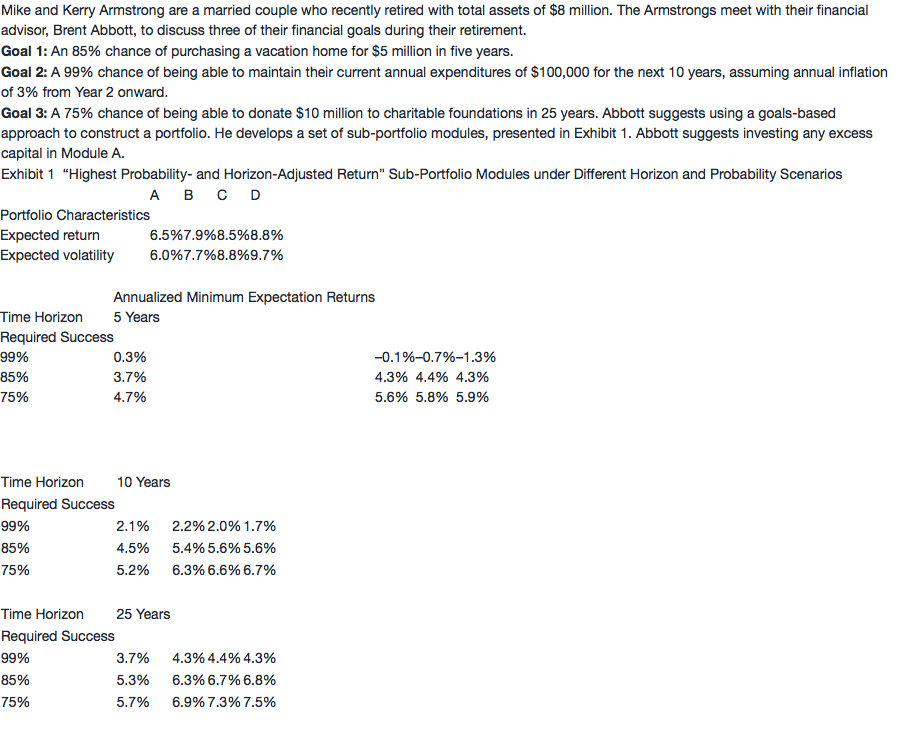

For Goal 1, which has a time horizon of five years and a required probability of success of 85%, Module C should be chosen because its 4.4% expected return is higher than the expected returns of all the other modules. The present value of Goal 1 is calculated as follows:

N = 5, FV = –5,000,000, I/Y = 4.4%; CPT PV = $4,031,508 (or $4.03 million)

So, approximately 50.4% of the total assets of $8 million (= $4.03 million/$8.00 million) should be allocated to Module C.

For Goal 2, which has a time horizon of 10 years and a required probability of success of 99%, Module B should be chosen because its 2.2% expected return is higher than the expected returns of all the other modules. The present value of Goal 2 is calculated as follows:

PV=$100,000/(1.022)1+$100,000(1.03)1/(1.022)2+$100,000(1.03)2/(1.022)3+...+$100,000(1.03)9/(1.022)10

PV = $1,013,670 (or $1.01 million)

So, approximately 12.7% of the total assets of $8 million (= $1.01 million/$8.00 million) should be allocated to Module B.

For Goal 3, which has a time horizon of 25 years and a required probability of success of 75%, Module D should be chosen because its 7.5% expected return is higher than the expected returns of all the other modules. The present value of

Goal 3 is calculated as follows:

N = 25, FV = –10,000,000, I/Y = 7.5%; CPT PV = $1,639,791 (or $1.64 million)

So, approximately 20.5% of the total assets of $8 million (= $1.64 million/$8.00 million) should be allocated to Module D.

Finally, the surplus of $1,315,032 (= $8,000,000 – $4,031,508 – $1,013,670 –$1,639,791), representing 16.4% (= $1.32 million/$8.00 million), should be invested in Module A following Abbott’s suggestion.

1.

1) goal 1 : module C

with 85% succussfully probobility and 5 year time horizon, using data from Exhibit 1, module C has the highest minimun expectation returns, which can minimize initial asset requirement.

2) goal 2 : module B

with 99% succussfully probobility and 10 year time horizon, using data from Exhibit 1, module B has the highest minimun expectation returns, which can minimize initial asset requirement.

3) goal 1 : module D

with 75% succussfully probobility and 25 year time horizon, using data from Exhibit 1, module D has the highest minimun expectation returns, which can minimize initial asset requirement.

2.

module A 16.5%, module B 12.62%, module C 50.38%, module D 20.5%

goal 1, choosing to allocate in module C, using minimize expectation return =4.4%, calculation PV=5/(1.044)^5 = 4.03m, 4.03/8 = 50.38%

goal 2, choosing to allocate in module B, using minimize expectation return=2.2%, calculation PV=100000/1.022+100000(1.03)/1.022^2+.....+100000(1.03)^9/1.022^10 = 1.01m 1.01/8=12.62%

goal 3, choosing to allocate in module D, using minimize expectation return =7.5%, PV=10/(1.075)^25 =1.64m,1.64/8=20.5%

excess capital investing in module A, = 8-4.03-1.01-1.64=1.32m 1.32/8= 16.5%