NO.PZ2024070701000002

问题如下:

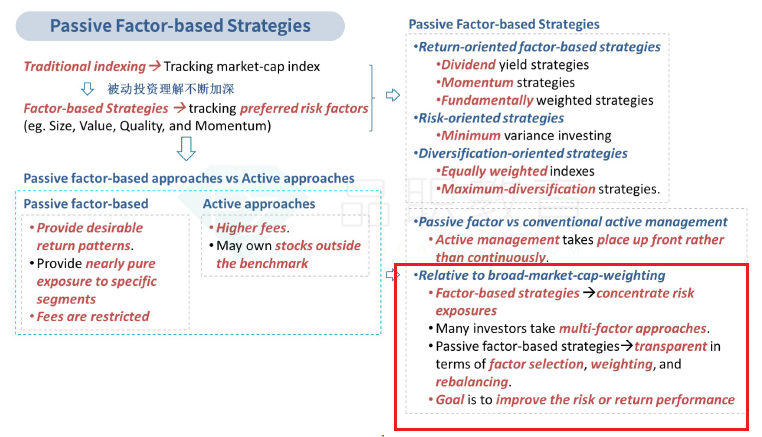

Stapleton then begins a description of factor-based strategies. These include common equity factors, such as value, size, and quality, and they can be used either in place of or to complement market-cap-weighted indexing. She points out that relative to market-cap weighting, factor-strategies tend to diversify risk exposures; are transparent in terms of factor selection, weighting, and rebalancing; but can be copied by other investors, which can reduce the advantages of a strategy.

When comparing factor-based strategies relative to the market-cap weighting of an index, Stapleton’s comments are most likely:

选项:

A.incorrect regarding transparency

correct

incorrect regarding risk exposure

解释:

Stapleton’s comment is incorrect regarding risk exposure. Relative to broad-market- cap- weighting, passive factor-based strategies tend to concentrate risk exposures, leaving investors exposed during periods when a chosen risk factor is out of favor.

A is incorrect. Stapleton’s comment is correct regarding transparency. Passive factor-strategies tend to be transparent in terms of factor selection, weighting, and rebalancing. The strategies can be easily replicated by other investors which can produce overcrowding and reduce the realized advantages of a strategy.

B is incorrect. Stapleton’s comment is correct regarding transparency but incorrect regarding risk exposure. Passive factor-based strategies tend to be transparent in terms of factor selection, weighting, and rebalancing. The strategies can be easily replicated by other investors which can produce overcrowding and reduce the realized advantages of a strategy. Relative to broad-market-cap-weighting, passive factor-based strategies tend to concentrate risk exposures, leaving investors exposed during periods when a chosen risk factor is out of favor.

factor selection为什么是transparent,因子用什么,用多少的权重,应该是不透明的,这部分为什么会容易被其他人复制呢