07:02 (2X)

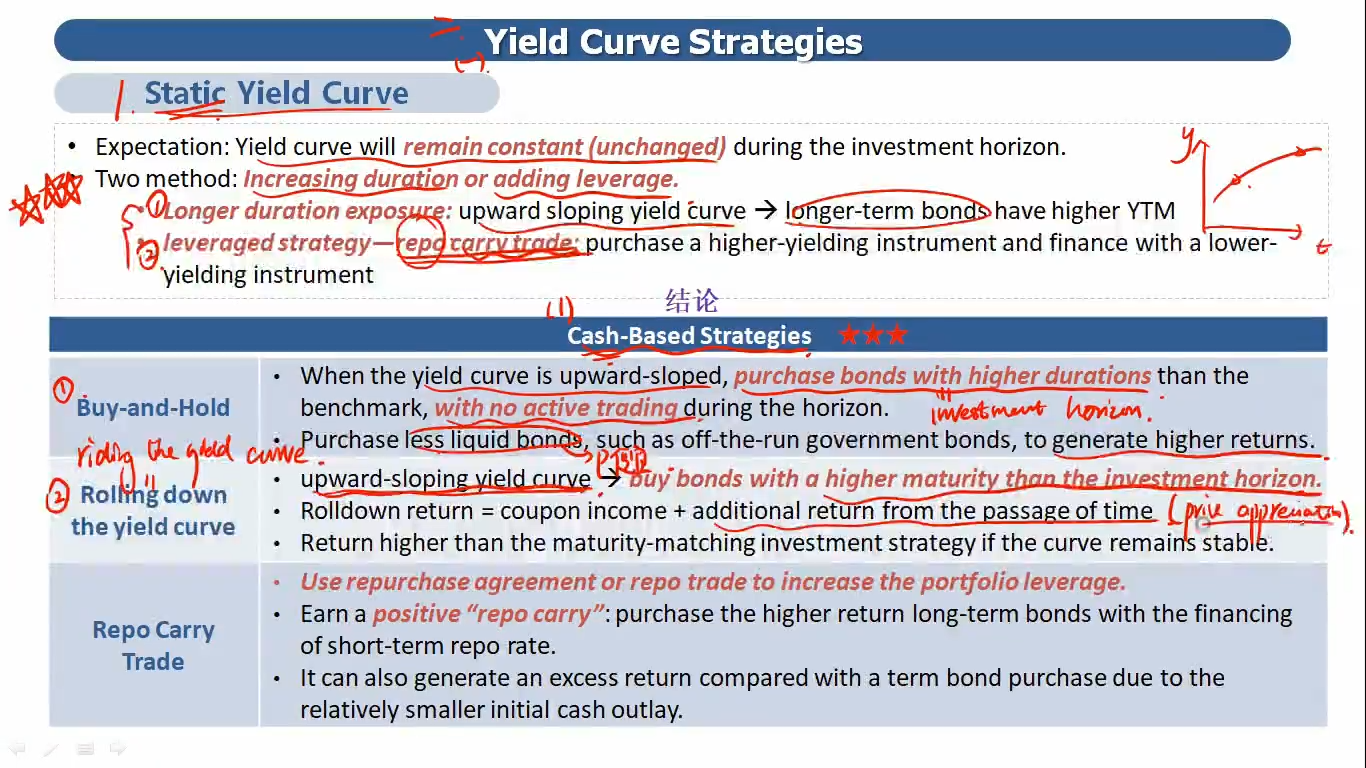

这里yield curve strategy里rollowdown return=coupon income+additional return from the passage of time(price appreciation),和core中讲的rollwdown return怎么不一样,core中的rolldown return就是(P1-P0)/P0,也就是上面等式的后半部分price appreciation.core中rolling yield=coupon income+the rolldown return.

还有credit strategy里面也有,rolldown return就是price appreciation,coupon income是另外算的。

以上不同章节的思路怎梳理,怎么区分?