NO.PZ2023010407000037

问题如下:

Mbalenhle Calixto is a global institutional portfolio manager who prepares for an annual meeting with the investment committee (IC) of the Estevão University Endowment. The endowment has €450 million in assets, and the current asset allocation is 42% equities, 22% fixed income, 19% private equity, and 17% hedge funds.

The IC’s primary investment objective is to maximize returns subject to a given level of volatility. A secondary objective is to avoid a permanent loss of capital, and the IC has indicated to Calixto its concern about left-tail risk. Calixto considers two asset allocation approaches for the endowment: mean–variance optimization (MVO) and mean–CVaR (conditional value at risk) optimization.

Determine the asset allocation approach that is most suitable for the Endowment. Justify your response.

选项:

解释:

请问老师,这样写可以么?我看答案写了好多

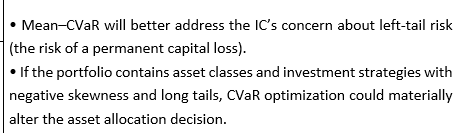

Mean–CVaR optimization is most suitable for the Endowment.

Alternative risk is usually not normal distribution. However, MVO is using standard deviation to measure risk which assumes the risk is normal distribution. So MVO is not suitable for the Endowment.

Mean–CVaR optimization is using CVaR measure risk which measures the average risk on the left-tail. So it is more suitable for the endowment.