NO.PZ2024102501000010

问题如下:

Rob Smith, as portfolio manager at Pell Tech University Foundation, is respon sible for the university’s USD3.5 billion endowment. The endowment supports the majority of funding for the university’s operating budget and financial aid programs, and it is invested in fixed income, public equities, private equities, and real assets.

The Pell Tech Board is conducting its quarterly strategic asset allocation review. T he board members note that although performance has been satisfactory, they have two concerns:

1. Endowment returns have underperformed in comparison to those of univer sity endowments of similar size.

2. Return expectations have shifted lower for fixed-income and public equity investments.

Smith attributes this underperformance to a lower risk profile relative to that of its peers because of a lower allocation to illiquid private equity investments. In response to the board’s concerns, Smith proposes an increase in the allocation to the private equity asset class. His proposal uses option price theory for valuation purposes and is supported by Monte Carlo simulations.

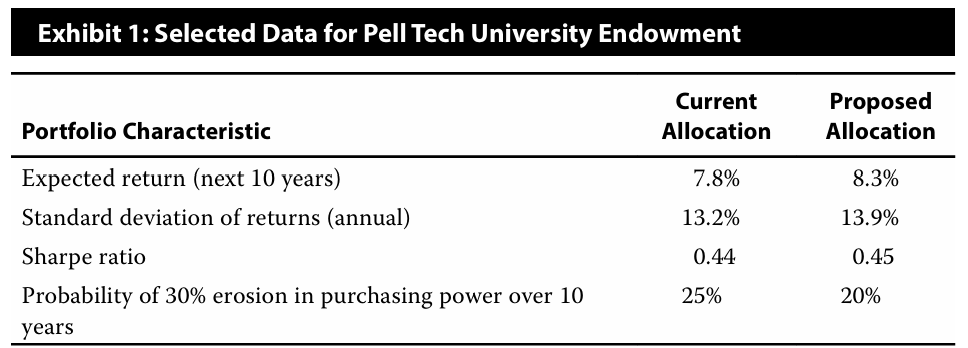

Exhibit 1 presents selected data on the current university endowment.

Discuss Smith’s method for estimating the increase in return expectations derived from increasing the endowment allocation to private equity.

选项:

解释:

Private equity is recognized as an illiquid alternative investment and could offer higher returns via a liquidity premium.

The illiquidity premium (also called the liquidity premium) is the expected compensation for the additional risk of tying up capital for a potentially uncertain time period. It can be estimated, as Smith has done, by using the idea that the size of a discount an investor should receive for such capital commitment is rep resented by the value of a put option with an exercise price equal to the hypothet ical “marketable price” of the illiquid asset as estimated at the time of purchase. Smith can derive the price of the illiquid private equity asset by subtracting the put price from the “marketable price.” If both the “marketable price” and the illiquid asset price are estimated or known, then the expected return for each can be calculated, with the difference in expected returns representing the illiquidity premium (in %).

机构IPS课后题这几个主观题这种类型的题目感觉很头疼,主观性很强,答不到点子上,不知道从何下手。