NO.PZ2024061801000078

问题如下:

A European call option has the following characteristics: S0= $50; X = $45; r = 5%; T= 1 year; and σ = 25%. Which of the following is closest to the value of the call?

选项:

A.

$1.88.

B.

$3.28.

C.

$9.06.

D.

$10.39.

解释:

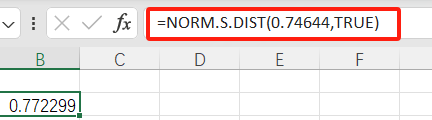

S0= $50; X = $45; r = 5%; T = 1 year; and σ = 25%.

d2= 0.74644 – 0.25 = 0.49644

from the cumulative normal table:

N(d1) = 0.7731

N(d2) = 0.6915*

c = 50(0.7731) – 45^e(–0.05)*0.6915= 9.055

如题这N(d1)不对吧…0.75不应该是0.7734吗