NO.PZ2023040401000049

问题如下:

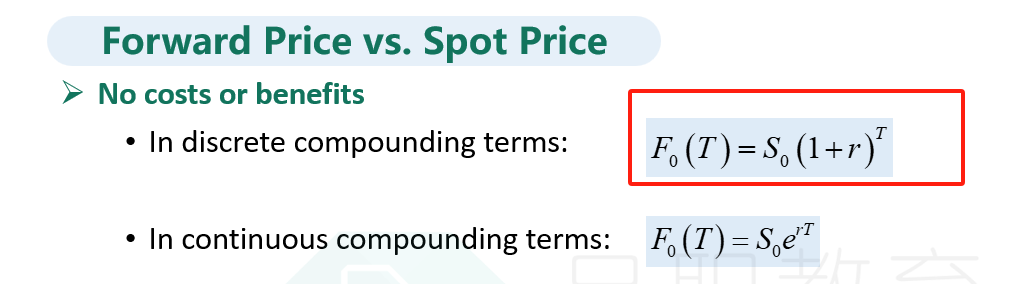

There are two forward contracts, contract 1 and contract 2, on the same underlying. The underlying makes no cash payments, does not yield any nonfinancial benefits, and does not incur any storage costs. Contract 1 expires in one year while contract 2 expires in two years. It is most likely that the price of contract 1:

选项:

A.is less than the price of contract 2.

is equal to the price of contract 2.

exceeds the price of contract 2.

解释:

The forward price is the spot price compounded at the risk-free rate over the life of the contract. Since Contract 2 has the longer life, compounding will lead to a larger value.

这道题应该这么理解,解析没看 明白,能否详细讲一下,谢谢