Your Answer:After-tax return:

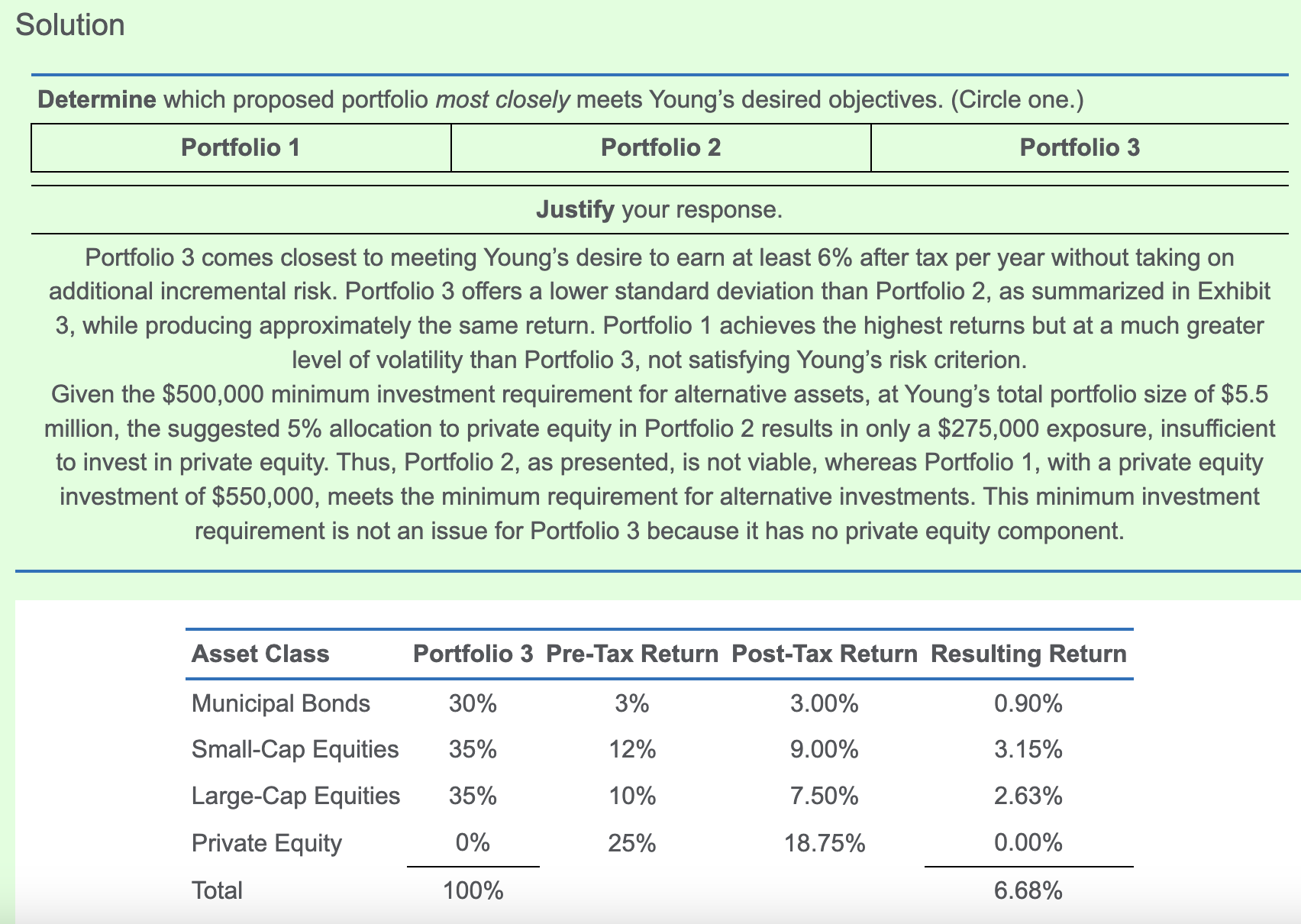

Portfolio 1: 9.1125%

Portfolio 2: 6.375%

Portfolio 3: 6.45%

All three portfolio meets the minimum return requirement of 6%

SFR for portfolio 1: 0.110

SFR for portfolio 2: 0.023

SFR for portfolio 3: 0.029

Portfolio 1 should be the one

这道题我做错了,回过头看看标准答案,感觉解题思路就错了。标准答案里的这句话“Portfolio 1 achieves the highest returns but at a much greater level of volatility than Portfolio 3, not satisfying Young’s risk criterion.” 是对应这篇case的最初就强调的 she places a high priority on retirement security and wants to avoid losing money in any of her three accounts.这个吗?

所以其实这道题就看一下波动率风险就把1剔除了?然后按照min investment amount选择的3?我看到“Young wants to earn at least 6.0% after tax per year”这句话就用SFR去计算了。

所以这道题就不应该考虑到SFR?