NO.PZ2022090602000051

问题如下:

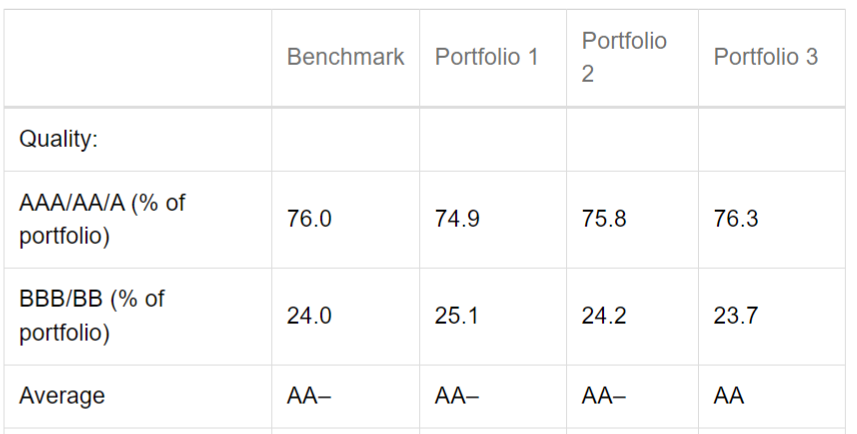

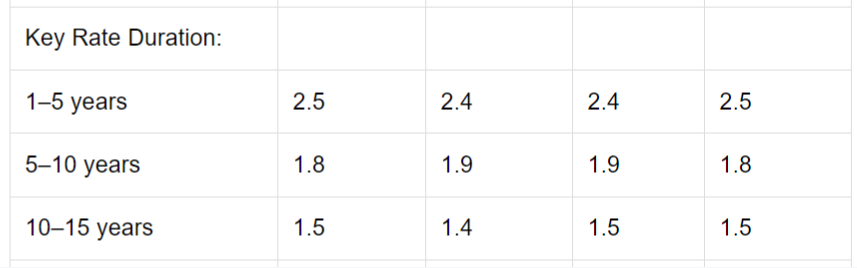

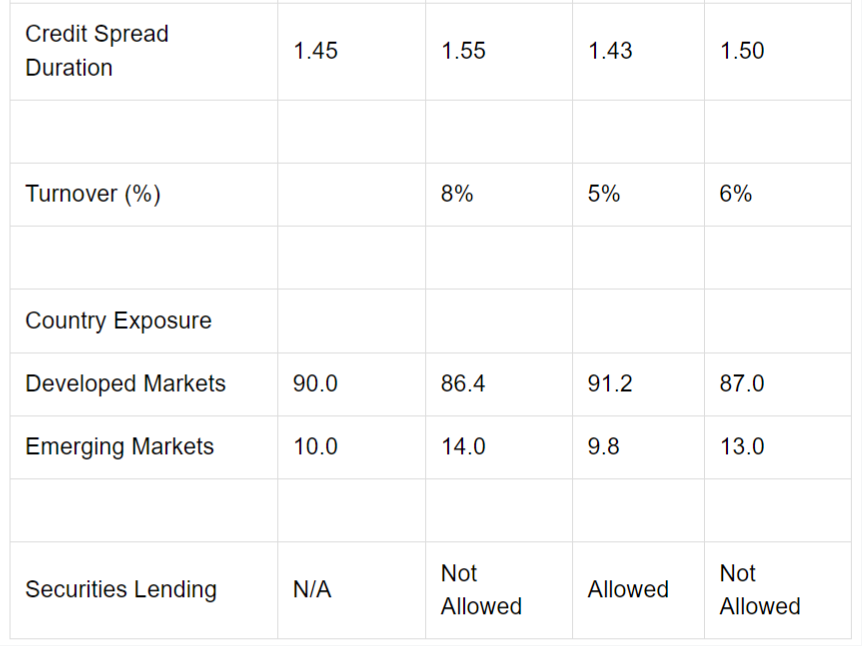

On page 2, Moynahan decides to outline the three total return approaches he utilizes to manage Reagan’s fixed-income portfolios. He puts together the following exhibit:

Exhibit 1 Features of Total Return Portfolios

How should Moynahan most likely label the management approaches for each of the portfolios described in Exhibit 1 on page 2 of his presentation?

Solutio

选项:

A.

Portfolio 1 = Active Management, Portfolio 2 = Pure Indexing, Portfolio 3 = Enhanced Indexing

B.

Portfolio 1 = Enhanced Indexing, Portfolio 2 = Pure Indexing, Portfolio 3 = Active Management

C.

Portfolio 1 = Active Management, Portfolio 2 = Enhanced Indexing, Portfolio 3 = Pure Indexing

解释:

A is correct. Moynahan should label the portfolios on page 2 as follows: Portfolio 1 = Active Management, which allows for larger risk factor mismatch to the benchmark. Portfolio 2 = Pure Indexing, which involves attempting to replicate a bond index as closely as possible. Portfolio 3 = Enhanced Indexing, which is closely linked to the benchmark but attempts to generate a modest amount of outperformance versus the benchmark.

B is incorrect because the ordering of portfolios given is incorrect. The correct ordering is: Portfolio 1 = Active Management, Portfolio 2 = Pure Indexing, Portfolio 3 = Enhanced Indexing.

C is incorrect because the ordering of portfolios given is incorrect. The correct ordering is: Portfolio 1 = Active Management, Portfolio 2 = Pure Indexing, Portfolio 3 = Enhanced Indexing.

我感觉都很接近 包括duration spread krd这些 不好判断