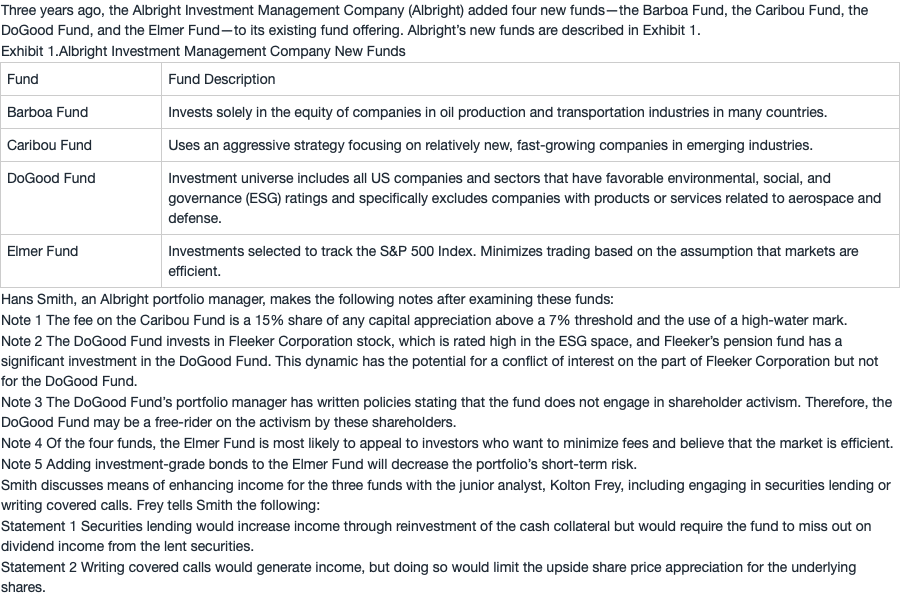

NO.PZ201809170400000107

问题如下:

Which of the notes regarding the Elmer Fund is correct?

选项:

A.

Only Note 4

B.

Only Note 5

C.

Both Note 4 and Note 5

解释:

A is correct. For passively managed portfolios, management fees are typically low because of lower direct costs of research and portfolio management relative to actively managed portfolios. Therefore, Note 4 is correct.

Note 5 is incorrect because the predictability of correlations is uncertain.

我是认为E基金是追踪标普500的被动投资,加入bond就会导致tracking error变大,短期风险加大,所以note 5 不对,请问老师这样是否合理?