NO.PZ2018031301000005

问题如下:

Viktoria Johansson is newly appointed as manager of ABC Corporation’s pension fund. The current market value of the fund’s assets is $10 billion, and the present value of the fund’s liabilities is $8.5 billion. The fund has historically been managed using an asset-only approach, but Johansson recommends to ABC’s board of directors that they adopt a liability-relative approach, specifically the hedging/return-seeking portfolios approach. Johansson assumes that the returns of the fund’s liabilities are driven by changes in the returns of index-linked government bonds. Exhibit 1 presents three potential asset allocation choices for the fund.

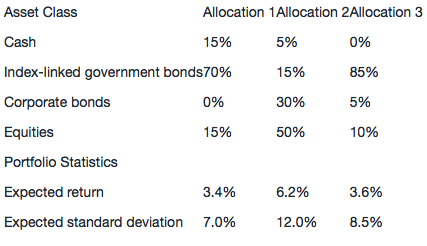

Exhibit 1 Potential Asset Allocations Choices for ABC Corp’s Pension Fund

Determine which asset allocation in Exhibit 1 would be most appropriate for Johansson given her recommendation. Justify your response.

选项:

解释:

■ Allocation 3 is

most appropriate.

■ To fully hedge the fund’s liabilities, 85% ($8.5 billion/$10.0 billion) of

the fund’s assets would be linked to index-linked government bonds.

■ Residual $1.5 billion surplus would be invested into a return-seeking portfolio.

The pension fund currently has a surplus of $1.5 billion ($10.0 billion – $8.5 billion). To adopt a hedging/return-seeking portfolios approach, Johansson would first hedge the liabilities by allocating an amount equal to the present value of the fund’s liabilities, $8.5 billion, to a hedging portfolio. The hedging portfolio must include assets whose returns are driven by the same factors that drive the returns of the liabilities, which in this case are the index-linked government bonds.

So, Johansson should allocate 85% ($8.5 billion/$10.0 billion) of the fund’s assets to index-linked government bonds. Te residual $1.5 billion surplus would then be invested into a return-seeking portfolio. Therefore, Allocation 3 would be the most appropriate asset allocation for the fund because it allocates 85% of the fund’s assets to index-linked government bonds and the remainder to a return seeking portfolio consisting of corporate bonds and equities.

我看答案前三句话并没有写出理由,只是陈述结论。这样也是可以的嘛?

我答题的时候只是写了因为国债风险低,没有写出答案的这句话,“The hedging portfolio must include assets whose returns are driven by the same factors that drive the returns of the liabilities, which in this case are the index-linked government bonds.”,这样可以吗?