NO.PZ2023100703000096

问题如下:

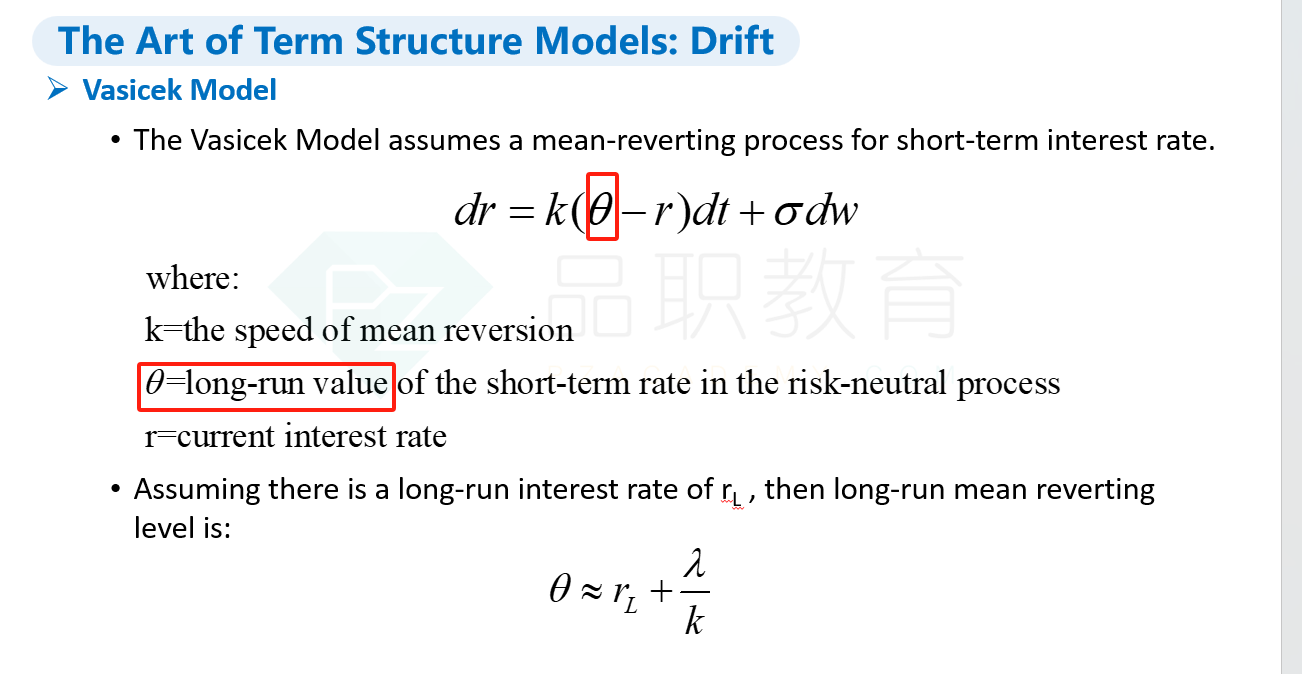

A hedge fund risk manager plans to adopt an interest rate term structure model whose risk neutral dynamics display mean reversion and a time-varying drift and consider Vasicek model as one of the candidates. Which of the following is correct about the Vasicek model?选项:

A.It gives rise to a downward-sloping term structure of volatility and allows for a time dependent drift. B.The short-term rates tend toward a long run equilibrium value and the expected value of the change in short-term rates is always zero over time. C.Shocks to short-term rates affect all rates equally, giving rise to parallel shifts. D.There is no mean reversion and the risk premium corresponds to a constant drift in Vasicek model.解释:

The Vasicek model incorporates mean reversion. The flexibility of the model also allows for risk premium, which enters into the model as constant drift or a drift that changes over time. In a model with mean reversion, shocks to the short rate affect short term rates more than longer-term rates and give rise to a downward-sloping term structure of volatility. B is incorrect as the drift of Vasicek model is not always zero. C is incorrect because shocks to the short rate affect short-term rates more than longerterm rates as Vasicek model comes with mean reversion. D is incorrect. The Vasicek model incorporates mean reversion. The flexibility of the model also allows for risk premium, which enters into the model as a constant drift or a drift that changes over time.term structure model 是为了计算哪个rate