NO.PZ202402070100000105

问题如下:

Which of the following choices best describes how SCSI could replicate a long risk-free bond return using a forward contract on CWI and call and put options on CWI?选项:

A.Short a forward contract on CWI, short a put option on CWI, and long a call option on CWI

B.Long a forward contract on CWI, long a put option on CWI, and short a call option on CWI

C.Long a forward contract on CWI, long a put option on CWI, and long a call option on CWI

解释:

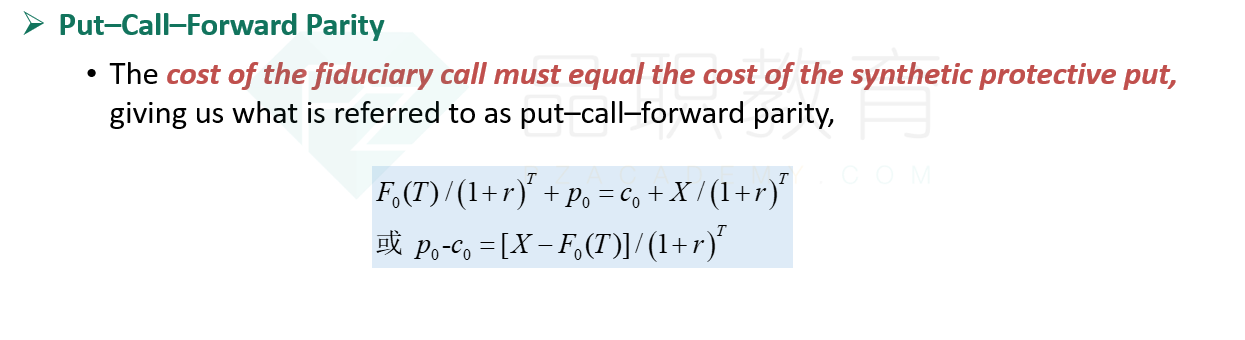

B is correct. Using the put-callforward parity equation as follows:

F0(T)(1 + r)-T +p0 = c0 + X(1 + r)-T

And rearranging to solve for therisk-free bond gives the following:

F0(T)(1 + r)-T +p0 - c0 = X(1 + r)-T.

The signs on the forward contract andput option positions are both positive, indicating long positions. The negativesign on the call option indicates a short position.

正确答案构建中是不是少了个long无风险利率?