NO.PZ202402070100000104

问题如下:

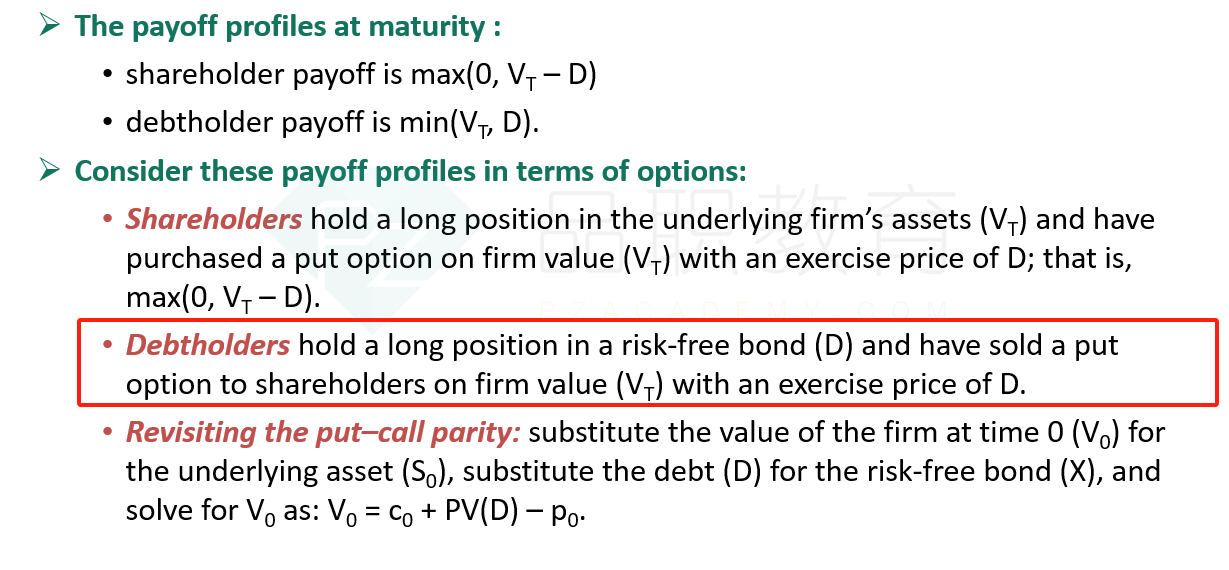

In her most recent research note on CWI, SCSI’s equity analyst specifically mentions an increase in CWI’s leverage ratio as a reason for her bearish outlook on the stock. Applying the put-call parity relationship to the value of the firm, which of the following statements most accurately describes the CWI outlook in terms of option pricing?选项:

A.The shareholder payoff has improved versus debtholders, because they have sold a put option on the firm value that has appreciated.

B.The debtholder payoff has deteriorated versus the shareholders, because they are effectively short a put option on the value of the firm equal to the value of debt, which has appreciated in value.

C.The shareholder payoff has improved versus the debtholders, because the debtholders have sold a call option on the firm’s assets to the shareholders.

解释:

The correct answer is B. Thedebtholder payoff has deteriorated versus the shareholders, because they areeffectively short a put option on the value of the firm equal to the value ofdebt, which has appreciated in value. The debtholder payoff is min(D, VT)= D –max(0, D – VT) and equals the debt face value (D) minusa put option on firm value (VT) with an exercise price of D. AnswerA is incorrect because the debtholders, not the shareholders, have sold a putoption. C is incorrect, because the shareholders own a call option, but it is notsold by the debtholders.

麻烦助教老师解释下这道题,有点看不懂解析了