NO.PZ2023102101000010

问题如下:

As a result of the credit crisis, the Basel Committee revised themarket risk framework and introduced a stressed VaR requirement. A bank usesthe internal models approach for market risk and has generated the followingrisk measures (in USD million) for the current trading book positions:

The supervisory authority has set the multiplicationfactors for both the VaR and stressed VaR values to 3. What is the capitalrequirement for general market risk? (Practice Exam)

选项:

A.

USD 1,665 million

B.

USD 3,977 million

C.

USD 6,132 million

D.

USD 8,502 million

解释:

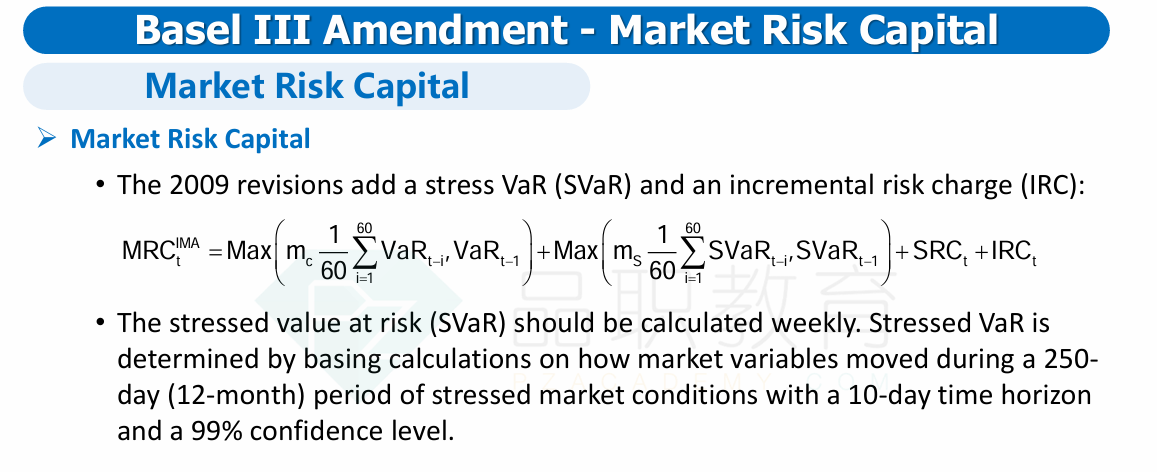

The revised market risk capital requirement is:

Market Risk Capital =max(VaRt-1, mc*VaR60-day Avg) + max(SVaRt-1,ms*SVaR60-day Avg)

= max(588, 3*555) + max(1345, 3*1489) = USD 6,132million

怎么做的,对应讲义哪里