NO.PZ2024011002000093

问题如下:

Due to significant changes in the marketplace, the demand for a company’s product has fallen and is not expected to recover to previous levels. The following information is related to the patent under which the product is produced:

Which of the

following statements is most accurate? The patent is impaired under:

选项:

A.IFRS only. B.U.S. GAAP only. C.both IFRS and U.S. GAAP.解释:

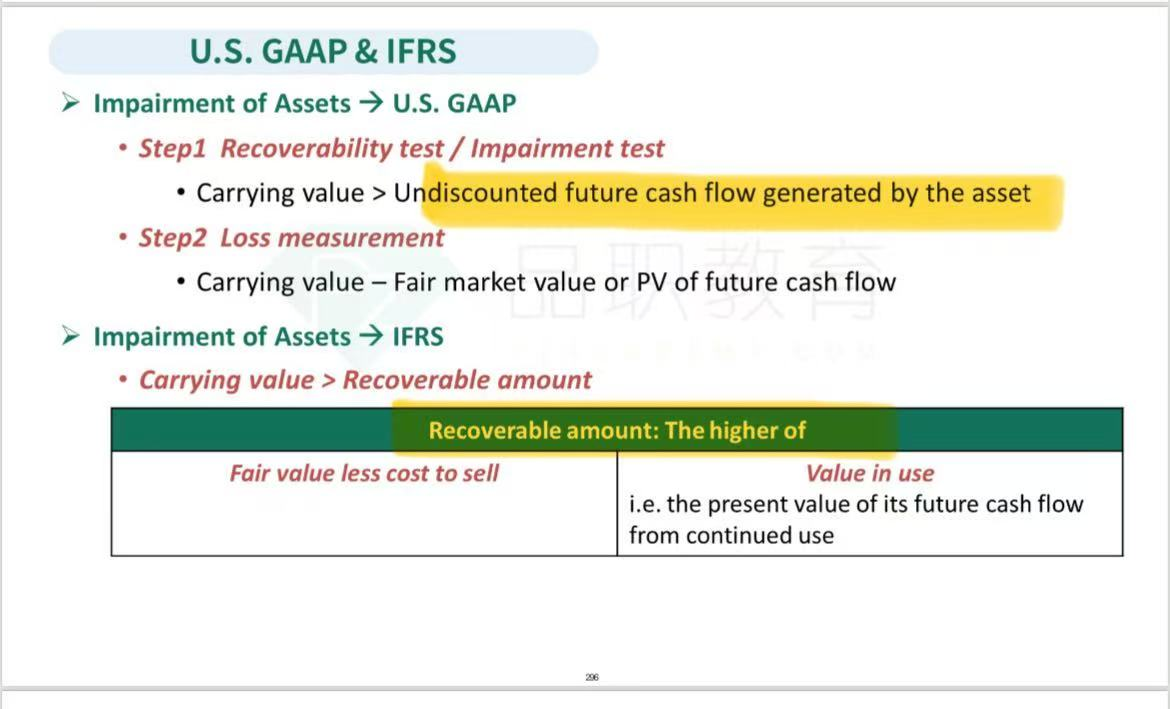

Under IFRS, first you must determine the recoverable amount that is the higher of:

- Value in use, which is the present value of the future cash flows: $32,000.

- Fair value less costs to sell: $34,000 - 4,000 = $30,000.

Therefore, the asset is impaired and should be written down to that amount.

Under U.S. GAAP, to assess impairment the carrying value ($36,000) is compared with the undiscounted expected future cash flows ($38,000).

In this case, the carrying value is lower, so the patent is not impaired.

如题