NO.PZ2023040401000047

问题如下:

Stocks BWQ and ZER are each currently priced at $100 per share. Over the next year, stock BWQ is expected to generate significant benefits whereas stock ZER is not expected to generate any benefits. There are no carrying costs associated with holding either stock over the next year. Compared with ZER, the one-year forward price of BWQ is most likely:

选项:

A.lower.

the same.

higher.

解释:

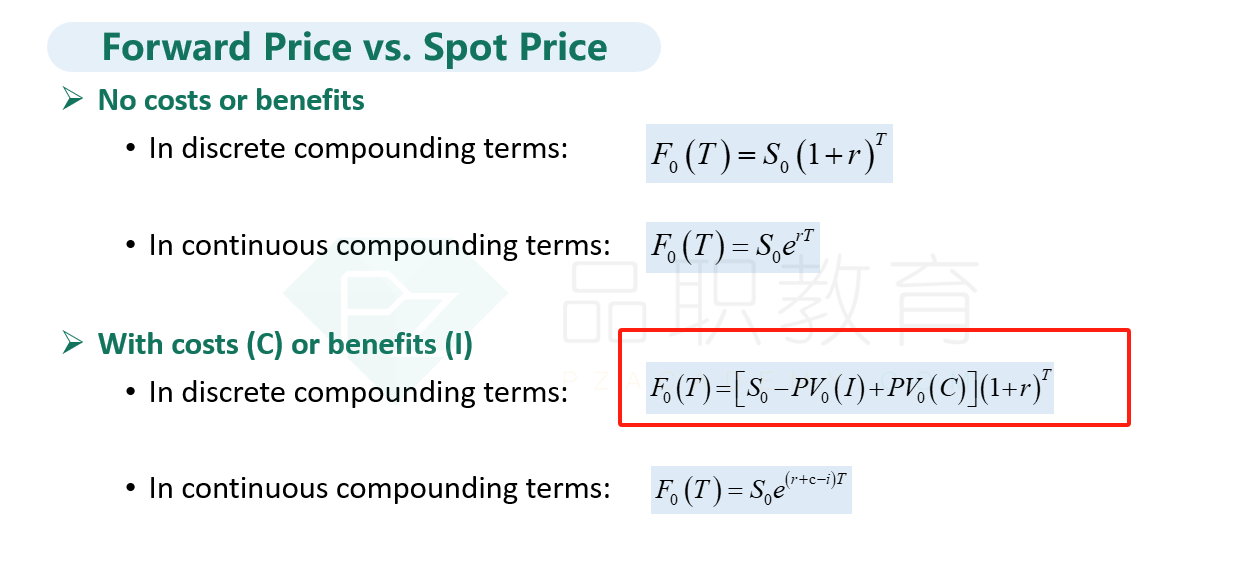

A is correct. The forward price of each stock is found by compounding the spot price by the risk-free rate for the period and then subtracting the future value of any benefits and adding the future value of any costs. In the absence of any benefits or costs, the one-year forward prices of BWQ and ZER should be equal. After subtracting the benefits related to BWQ, the one-year forward price of BWQ is lower than the one-year forward price of ZER.

如题