NO.PZ2023061903000027

问题如下:

Q. The JPY/AUD spot exchange rate is 82.42, the Japanese yen interest rate is 0.15 percent, and the Australian dollar interest rate is 4.95 percent. If the interest rates are quoted on the basis of a 360-day year, the 90-day forward points in JPY/AUD would be closest to:选项:

A.–377.0.B.–97.7. C.98.9.

解释:

B is correct. The forward exchange rate is given by:

The forward points are as follows:

100 × (F × S) = 100 × (81.443 – 82.42) = 100 × (–0.977) = –97.7.Because the spot exchange rate is quoted with two decimal places, the forward points are scaled by 100.

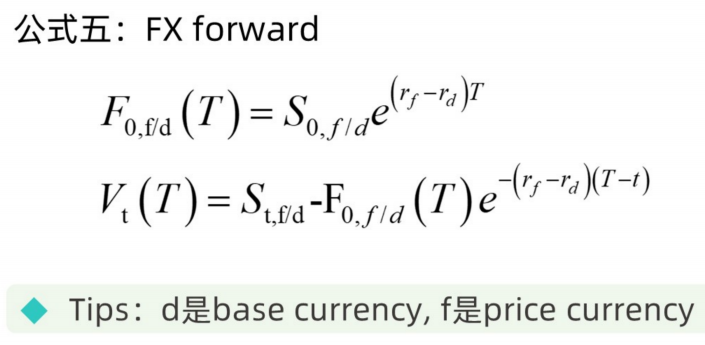

那个带e的公式是什么时候用的?