NO.PZ2023091601000099

问题如下:

A risk manager at a hedge fund wants to

conduct a simulation to forecast the stock price of a particular company at a

future date. The manager aims to achieve this by simulating the values of a

European option and an Asian option on the company’s stock that mature on the

specified future date, and considers several methods to improve the accuracy of

the simulation. Which of the following statements is correct regarding the

methods typically used to reduce sampling error?

选项:

A.Antithetic

variables introduce a set of random variables that are positively correlated

with the simulation variables to reduce the number of replications.

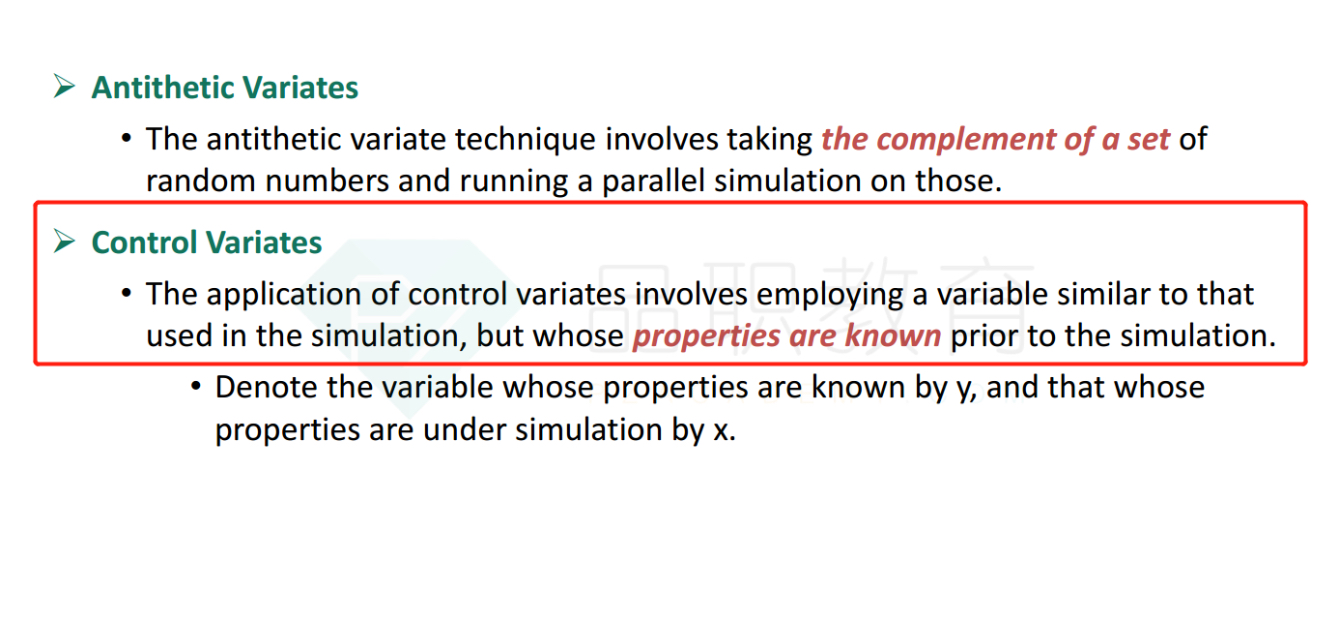

Control variates

and antithetic variables both reduce bootstrapping sampling variability for a

given number of replications.

The use of control

variates is limited to simulations in which there is a closed-form solution

with which to compare the simulated outcome.

The application of

control variates involves employing a variable with a mean of zero and a strong

positive correlation with the simulated values.

解释:

D is correct. This is the definition of

control variates.

A is incorrect. Antithetic variables have to

be negatively correlated to the simulation variables in order to reduce the

Monte Carlo sampling variability for a given number of replications, or to

reduce the number of replications while retaining the current level of sampling

variability.

B is incorrect. Both techniques can be used

simultaneously, and the purpose of the two techniques is to reduce Monte Carlo

sampling error – not bootstrapping error.

C is incorrect. In the first place, Monte

Carlo simulation is evidently most useful when no analytical or closed-form

solution exists – for example, when pricing complex exotic options. Hence,

using control variates to reduce sampling error in Monte Carlo simulation would

consequently be helpful in cases where no analytical solution exists.

课件的PDF不太好搜索,请问一下这个是哪一章的知识点呢?