NO.PZ2023091601000079

问题如下:

Which of the following statements about the exponentially

weighted moving average (EWMA) model and the generalized autoregressive

conditional heteroskedasticity(GARCH(1,1)) model is correct?

选项:

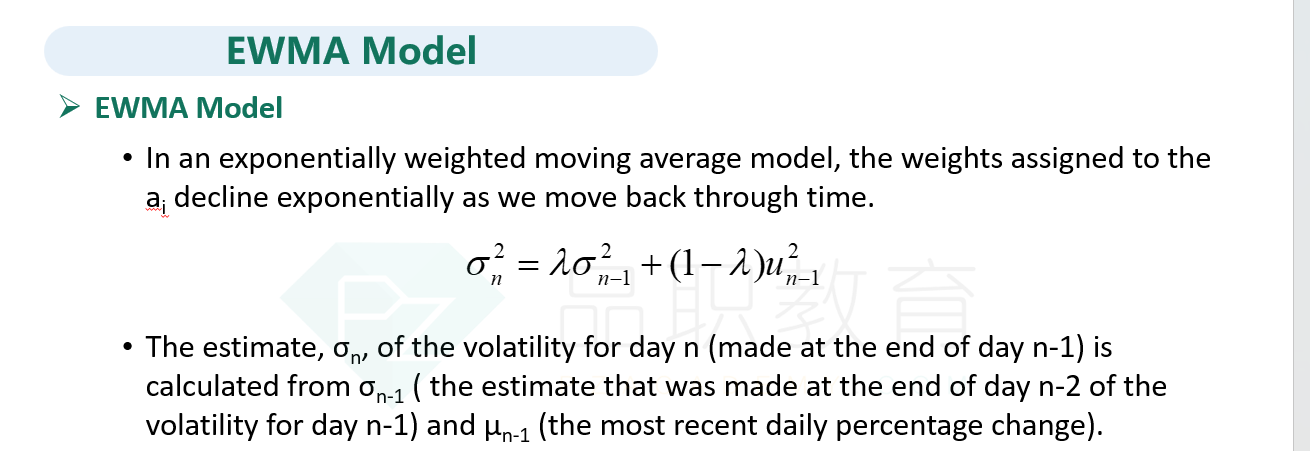

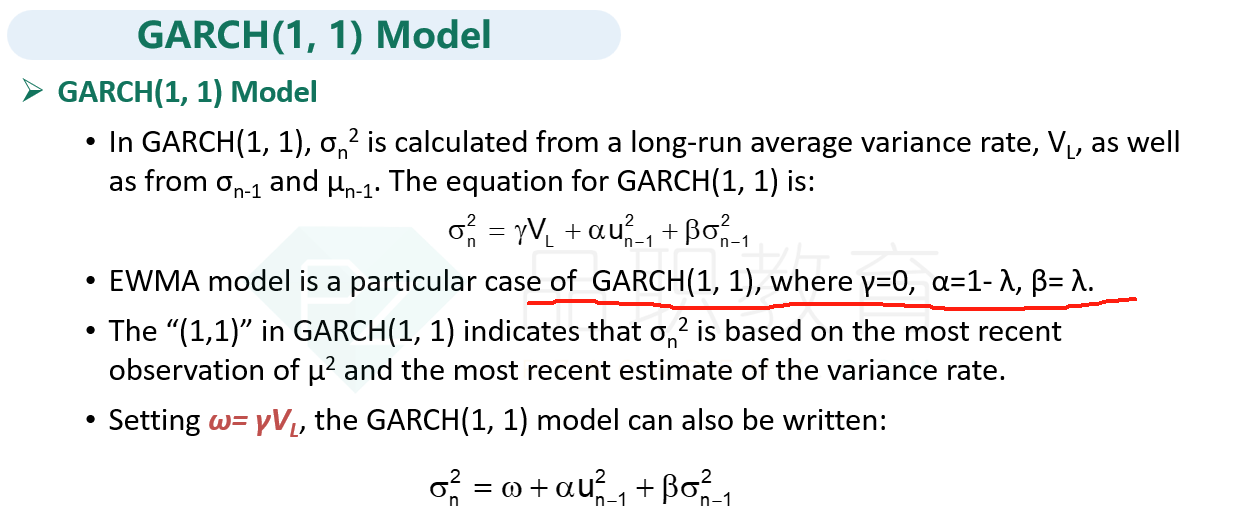

A.The EWMA model is a special case of the GARCH(1,1) model

with the additional assumption that the long-run volatility is zero.

A variance

estimate from the EWMA model is always between the prior day’s estimated

variance and the prior day’s squared return.

The GARCH(1,1) model always assigns less weight to the

prior day’s estimated variance than the EWMA model.

A variance estimate from the

GARCH(1,1) model is always between the prior day’s estimated variance and the

prior day’s squared return.

解释:

The EWMA estimate of

variance is a weighted average of the prior day’s variance and prior day

squared return.

A为什么不对?