NO.PZ2024021803000068

问题如下:

For a forward contract with a value of zero, a situation where the spot price is above the forward price is best explained by high:

选项:

A.interest rates.

B.storage costs.

C.convenience yield.

解释:

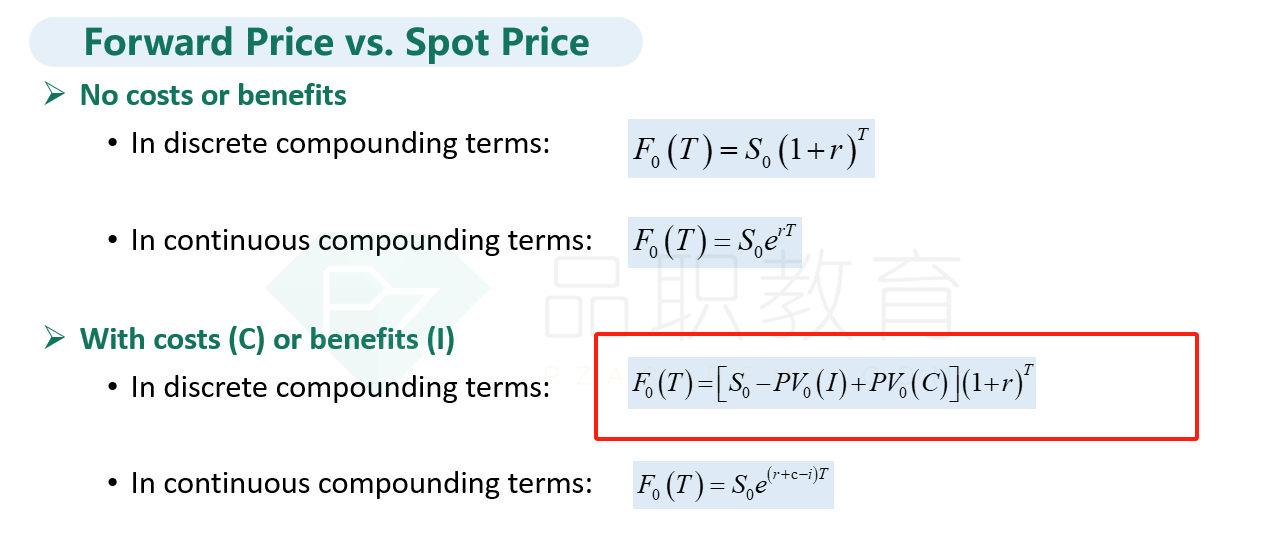

C is correct. If

the convenience yield is high, holding the underlying confers large benefits,

thus the spot price can exceed the forward price for a forward contract with a

value of zero. Based on the formula Vt(T) = St –PVT(I)+PVT(C)–

F0(T)(1 + r)–(T–t)and an initial value Vt(0)

of zero, large benefits PVT(I) explain why the spot price can exceed

the forward price.

A is incorrect.

High interest rates make the forward contract more valuable. Thus, the forward

rate is above the spot rate.

B is incorrect.

High storage costs make the forward contract more valuable. Thus, the forward

rate is above the spot rate.

老师能解析下这道题目吗?不是很明白