NO.PZ2019052801000129

问题如下:

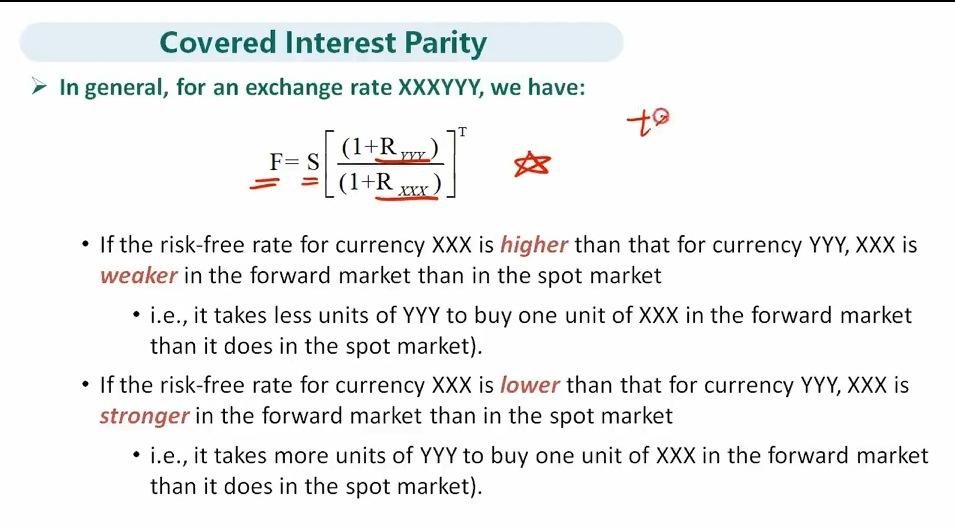

An Chinese trade company mainly exports goods to US and gives 90 days credit term for US companies. The payment is settled in USD. The Chinese company worries that the USD will depreciate and would like to hedge the downside risk by entering a short forward. Domestic risk-free rate is 4% and foreign risk-free rate is 2%. The current spot rate is 6.7523¥per $. What is the price of the forward contract?

选项:

A.6.3827.

B.6.7847.

C.6.5827.

D.6.6827.

解释:

B is correct.

考点:Foreign Exchange Risk

解析:中国公司会在90天后收到美元,但是担心未来美元会下跌,所以签订了一个short USD forward作为对冲。远期合约的价格应该等于:

我在看这期视频课的时候,Estimating Foreign Exchange Risk,没有定价模型啊?请问FX 期货定价模型在哪期课件里?