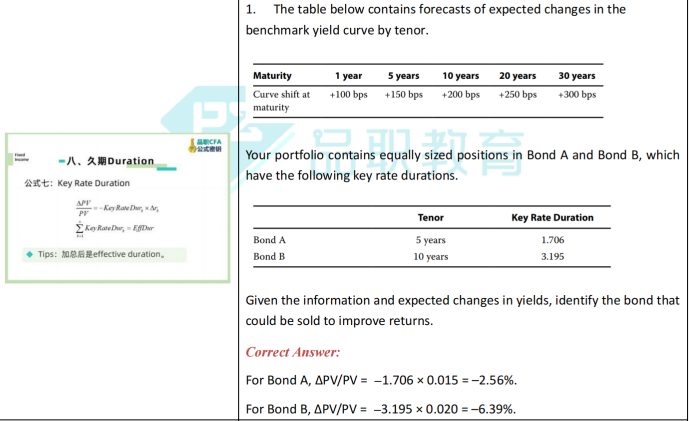

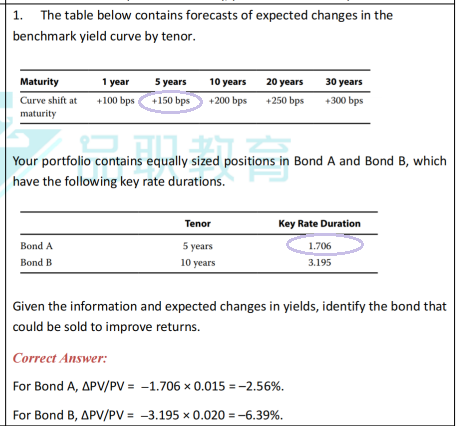

The table below contains forecasts of expected changes in

the benchmark yield curve by tenor . Your portfolio contains equally sized positions in Bond A and Bond B, which have the following key rate durations,Given the information and expected changes in yields. identify the bond that could be sold to improve returns.参考答案 -2.56%, -6.39% 。 这题和答案分别说的是什么,看不懂